Well Cost | Quarterly / Earnings Reports | Second Quarter (2Q) Update | Production Rates | Forecast - Production | Capital Markets | Capital Expenditure

Encana Adds $100 Million To CapEx, Eagle Ford Well Cost Increases

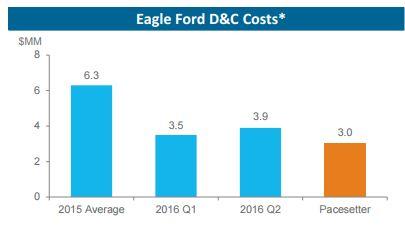

Encana just release its Q2, 2016 data. A quick read shows two interesting pieces of data. One, Encana saw its Eagle Ford Well cost rise by $400,000 to $3.9 million in Q2-2016, up from Q1-2016. The company also annouced it was spending an additional $100 million, however it will have no impact on production or number of wells.

Encana is also raising its 2016 production guidance. The company expects to use proceeds from announced dispositions to further strengthen its balance sheet and increase its capital investment into high return opportunities in its core four assets.

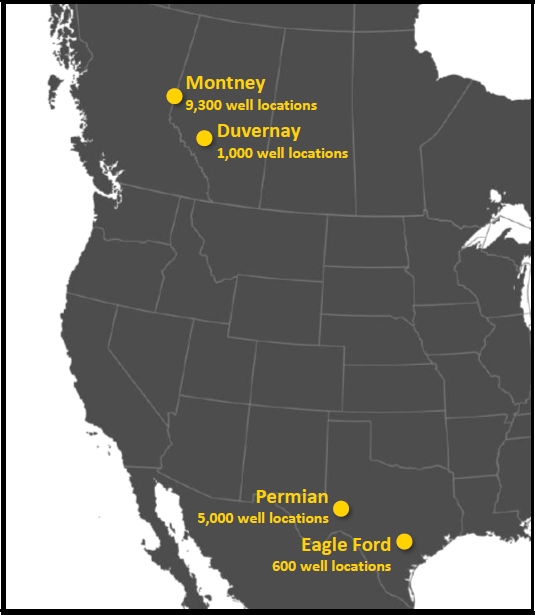

Operating Areas

Key Points:

- Increase to 2016 capital program

- Permian - completing the Midland Basin's first 14-well pad. This peaked at 12,000 BOE/d and is currently producing over 10,000 BOE/d gross.

- Eagle Ford - Wells Cost rise from $3.5M (5,000 ft Lateral) to $3.9 Million in Q2 (5,000 ft Lateral)

Highlights from the quarter include:

- 95 percent of capital invested in high return wells in the core four assets; the Permian, Eagle Ford, Duvernay and Montney

- maintained scale in the core four assets which delivered 268,300 barrels of oil equivalent per day (BOE/d), representing 73 percent of the company's 368,300 BOE/d total production

- new Permian 14-well pad peaked at 12,000 BOE/d and is currently producing over 10,000 BOE/d gross

- announced Gordondale and DJ Basin divestitures are expected to close by the end of July 2016

Doug Suttles, Encana President & CEO, said: "We are one of the lowest cost, highest performing operators in each of our core four plays. Our success in capturing significant capital efficiency gains continues to increase our returns. By reinvesting savings and modestly increasing capital, we are adding 50 percent more drilling and completions activity to our 2016 program."

"We expect to use proceeds from announced divestitures to strengthen our balance sheet and modestly increase our 2016 capital program. We anticipate this additional activity will deliver approximately 13,000 BOE/d of production from our core four assets in the fourth quarter of this year and between 30,000 to 35,000 BOE/d in 2017, of which approximately 75 percent will be liquids," added Suttles.

Core Areas

Encana beat its 2016 drilling and completions cost reduction targets in the first quarter. In the second quarter the company continued to lower drilling and completion costs across its four core assets and they are now over 30 percent lower compared to the 2015 full-year average. In addition, Encana delivered new pacesetter performance and has a track record of rapidly converting pacesetter benchmarks into average costs.

In the Permian, Encana built on its track record as a leading innovator by completing the Midland Basin's first 14-well pad. This peaked at 12,000 BOE/d and is currently producing over 10,000 BOE/d gross. In addition, it delivered a 10 percent quarter-over-quarter reduction in average drilling and completions costs. These costs are 31 percent lower than the full-year 2015 average. Encana is now the second largest producer in the core of the Midland Basin.

In the Eagle Ford, Encana delivered a new pacesetter well at a cost of $3 million. Average drilling and completions costs in the second quarter in the play were 38 percent lower than the 2015 average. However the company saw its eagle ford average well cost increase to $3.9 million up from $3.5 million in Q1.

In the Duvernay, Encana delivered a $6.8 million pacesetter well. The second quarter average drilling and completions costs were approximately 40 percent lower than the company's 2015 average.

In the Montney, Encana continued to deliver strong results from its condensate-rich wells in the Tower, Dawson South and Pipestone areas. Combined, these areas offer a potential inventory of almost 6,000 condensate-rich well locations. Second quarter average drilling and completions costs were down 14 percent compared to the first quarter and 33 percent lower than the full-year 2015 average.

Continued cost and capital efficiency and disciplined balance sheet management

Encana continued to capture significant cost savings during the second quarter. As a result, the company is lowering its guidance for transportation, processing and operating costs by $100 million for the year. Encana expects the full-year benefit of these savings will be even greater in 2017.

Encana is reinvesting savings from continued capital efficiency improvements and expects to use a portion of proceeds from its Gordondale and DJ Basin divestitures to increase its 2016 capital program by $200 million. As a result, after adjusting for the Gordondale divestiture, the company is increasing its 2016 production guidance and expects fourth quarter exit production decline from its core four assets to be cut from 10 percent to five percent. Encana's Gordondale and DJ Basin divestitures are expected to close by the end of July delivering proceeds of approximately $1.1 billion.

Second quarter results

Encana's core four assets contributed 268,300 BOE/d or approximately 73 percent of total second quarter production of 368,300 BOE/d. Total liquids production averaged 132,000 barrels per day (bbls/d) and natural gas production averaged 1.4 billion cubic feet per day (Bcf/d).

Encana generated second quarter cash flow of $182 million or $0.21 per share, compared to $181 million or $0.22 per share in the second quarter of 2015. The company recorded second quarter operating earnings of $89 million or $0.10 per share compared to an operating loss of $167 million or $0.20 per share in the second quarter of 2015. The second quarter net loss of $601 million, or $0.71 per share, is largely attributable to non-cash items such as after-tax ceiling test impairments and an after-tax unrealized hedging loss.

Hedging

As at June 30, 2016, Encana has hedged approximately 78 percent of its remaining expected 2016 oil and condensate production at an average price of $55.91 per barrel and 86 percent of expected natural gas production at an average price of $2.63 per thousand cubic feet (Mcf).

Encana has about 15,500 bbls/d of expected 2017 crude and condensate hedged using WTI fixed price contracts at an average price of $49.49 per bbl. In addition, the company has hedged 10,000 bbls/d under WTI three-way options for the second half of 2017. The company also has 300 million cubic feet per day (MMcf/d) of expected 2017 natural gas production hedged under three-way options and 350 MMcf/d using NYMEX fixed price contracts for the first quarter of 2017.

| Category | 2023 | 2024Est. Initial | Updated 2024 Guidance | %Difference (2023 vs 2024) |

| Total Capital Expenditure($mm) |

|

|

|

|

| Production Oil(bbls/d) |

|

|

|

|

Related Categories :

Second Quarter (2Q) Update

More Second Quarter (2Q) Update News

-

Saturn Oil & Gas Second Quarter 2022 Results

-

Empire Petroleum Second Quarter 2022 Results

-

ProFrac Holding Corp. Second Quarter 2022 Results

-

InPlay Oil Corp. Second Quarter 2022 Results

-

Vermilion Energy Inc. Second Quarter 2022 Results

Canada News >>>

-

Seventeen (17) E&Ps; To Use 47 Frac Crews To Complete 2,800 Wells In 2024

-

These Permian Operators Plan to Complete/Frac 2,100 Wells IN 2024

-

Large E&P Chops Permian/Anadarko Basin Frac Activity by 30% In 2024

-

Permian E&P Ups 2024 Well Completed by +27% vs. 2023

-

Contrary to The Noise, U.S. Oil Production will Likely Growth 4-5% In 2024; A look Inside -

Gulf Coast - South Texas News >>>

-

New Permian E&P Company Score Capital; On The Hunt For Assets -

-

Chevron To Cut D&C Activity in U.S. Shale In 2024; Here is Where. -

-

An Early Look at Company 2024 Capital & Development Plans

-

EOG Resources Reports Third Quarter 2023 Results

-

A Look at Capital Spending By Company In First Half 2023; Budget Exhausion?