Exploration & Production | Seismic | Capital Markets | Capital Expenditure | Drilling Program

Sterling Resources Updates Breagh and Cladhan Progress

Sterling Resources Ltd. has announced an update of development activity at the Breagh and Cladhan fields in the UK North Sea, planned exploration and appraisal activity for 2014 and 2015, and a financial update.

Breagh

With the recent success of the A07 and A08 hydraulic stimulations, Sterling and the operator, RWE Dea (UK) Ltd, are progressing plans for the drilling of four additional wells (12 wells in total) from the Breagh Alpha platform.

This program will be subject to well planning and analysis of the 3D seismic acquired earlier in 2014, the preliminary interpretation of which is expected to be available in Q1 2015, and assumes hydraulic stimulation of all wells. Wells A09 and A10 are expected to be drilled in the second half of 2015.

The drilling program is expected to continue during 2016 with new wells A11 and A12, and the likely sidetrack and stimulation of one or two existing lower performance wells.

Plans for Breagh Phase 2 will be reconsidered following the 3D seismic interpretation in 2015 and the accumulation of production history. With this new data, Sterling expects the field development plan to be updated with the intention of submitting the revised plan towards the end of 2015 for anticipated approval during 2016.

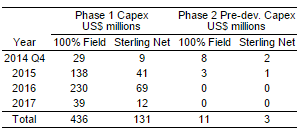

Capital expenditure profiles for the remainder of Breagh Phase 1 development and for Phase 2 pre-development sanction, reflecting the drilling and stimulation plans outlined above (with two existing lower performance wells being sidetracked and stimulated) together with onshore compression to be installed over 2015-2017, are set out in the table below on a cash basis. The costs of wells A11 and A12 and of the sidetrack and stimulation of existing lower performance wells are Sterling estimates. Sterling expects to develop these estimates along with RWE as part of the 2016 work program.

Following the start-up of well A07 in early August 2014 up until mid-October, production uptime (excluding planned shutdowns for drilling rig-related activity) has been reliable at in excess of 96 percent. The field had been producing at approximately 113 million cubic feet of sales gas per day with wells A01-A07 onstream, prior to a field shutdown in mid-October for an unscheduled inspection of the condensate stabilization system at the Teesside Gas Processing Plant. The shutdown has progressed well and production is expected to recommence in late October after a shutdown of approximately 12 days. Well A08 is now expected to come onstream in early November shortly after the restart of field production.

Sterling has revised its reservoir simulation model to reflect the results of the A07 and A08 hydraulic stimulations and production history to end September 2014. This modelling work has not been reviewed by RWE. For 2014, Sterling now expects average sales gas production for 100 percent of Breagh of 87 MMscf/d (26 MMscf/d net to Sterling), compared to the guidance issued on July 1, 2014 of 91 MMscf/d (27 MMscf/d net to Sterling) primarily as a result of the delay in hook-up of well A08 and the additional shutdown at the TGPP during this month. For Q4 2014, average expected sales gas production for 100 percent of the field is now 122 MMscf/d (36 MMscf/d net to Sterling) with an end 2014 exit rate of 145 MMscf/d (43 MMscf/d net to Sterling). In addition to gas production, condensate is expected to be produced at an average condensate-gas ratio of 3.3 barrels per MMscf.

Average expected sales gas production for 2015 for 100 percent of Breagh is now 112 MMscf/d (33 MMscf/d net to Sterling), very close to the previous guidance issued on July 1, 2014 of 111 MMscf/d (33 MMscf/d net to Sterling).

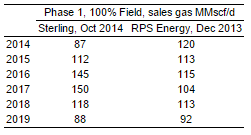

Over the next five years, with the work program set out above, Sterling estimates significantly higher production than for the 2P (proven plus probable) case prepared by RPS Energy in its report "Executive Summary Reserves and Resources of the Breagh Gas Field as at December 31, 2013" dated April 29, 2014. Sterling's profile assumes 12 wells in total and the sidetrack and stimulation of two existing lower performance wells as described above. The assumptions adopted by RPS Energy at the end of 2013 included 10 wells and no hydraulic stimulation. Estimated annual average sales gas production over 2014-2019 for these two cases is set out in the table below. For the period 2015-2019, Sterling's revised profile shows an incremental net sales gas production of 8.3 Bcf (average incremental 4.6 MMscf/d over the period) above the RPS end 2013 profile. The revised Sterling profile has not been reviewed by RWE.

Due to the continued uncertainty related to the timing and development concept of Breagh Phase 2, production and capex profiles for Phase 2 have not been prepared by Sterling at this point.

Cladhan

The first production well (P1) has been drilled and completed, encountering more and higher quality sands than predicted. The water injection well (W1) has been drilled and encountered the high quality down-dip reservoir sands evident from the 210/29-4Y appraisal well drilled by Sterling during 2010. This will complete the producer/injector pairing in the Cladhan main channel area. The Transocean 'John Shaw' semi-submersible drilling rig will shortly be moving to the second production well, P2, which has been suspended in order to use information from W1 to optimize the down-hole location of P2 (which is positioned between, but to the south of, the P1 and W1 wells). It is expected that P2 will be completed in December 2014.

First oil is now forecast for Q3 2015. Slippage from the previous estimate of Q2 2015 has primarily been driven by changes in the subsea work scope and a decision to defer elements of this scope into spring 2015 to mitigate the potential for adverse weather impact during the winter period. Latest project cost forecasts show an increase of 12 percent from the original budget and pay-out of the second (2013) TAQA carry is now expected during Q3 2016 at forward curve oil prices. Sterling's equity interest is therefore expected to remain at 2.0 percent throughout 2015, rising to 13.8 percent after pay-out of the second carry. The development cost for the 2.0 percent interest is likely to exceed the available funding from the first (2012) TAQA carry by approximately US$2 million.

Sterling's average net production in thousands of barrels per day, after reflecting pay-out of the second TAQA carry, for the next 5 years is set out in the table below. The profile has been generated by Sterling based on the 2P (proven plus probable) case in the RPS Energy report "Executive Summary Reserves and Resources of the Cladhan Oil Field as at December 31, 2013" dated April 29, 2014, reflecting the impact of the delay to start-up and to the pay-out of the second TAQA carry.

Exploration and Appraisal Activity

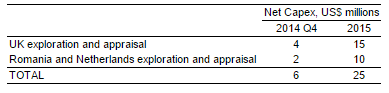

Sterling has revised its exploration and appraisal plans for the UK North Sea and offshore Romania. In the UK, the Crosgan appraisal well in block 42/15a (Sterling 30 percent) is expected to spud within the next few days; the cost (including a production test) is likely to be incurred on a cash basis partly in the same quarter and partly in Q1 2015. In 2015, the only UK E&A well planned is a well in blocks 21/30f and 22/01c containing the Beverley prospect and the Belinda and Evelyn oil discoveries (Sterling 20 percent). The net cost of this well will be largely covered by a carry arrangement. The Niadar exploration well in block 49/19b is now expected to be drilled in 2016.

In Romania, the equity sell-down process on Sterling's Luceafarul, Muridava, Midia and Pelican blocks is now underway. Sterling's only outstanding commitment exploration wells in Romania are one well on the Luceafarul block and two wells on the Muridava block (Sterling 50 percent and 40 percent respectively). One of these three wells is likely to be drilled in Q4 2015 and the other two in Q1 2016. Depending on the outcome of the equity sell-down process, one or two exploration wells may be drilled on the Midia block (Sterling 65 percent) but these are not commitment wells and will only be drilled if financing is available.

For the purposes of the capex estimates below, management has indicatively calculated the net cost on a cash basis in each of the Romanian blocks at half the current equity interest (together with a cash receipt in respect of half the past 3D seismic costs on the Midia, Pelican and Luceafarul blocks), prior to the benefit of expected promotes.

Financial Update

The Company continues with discussions to address the funding shortfall in late 2014 and for provide financing to cover the first half of 2015. The Company faces a concentration of Breagh drilling capex and E&A expenditure in the second half of 2015, by which time it is intended to have refinanced the UK senior secured bond, possibly via a reserves based loan in the bank market.

As at September 30, 2014 the Company had US$56.7 million of total cash and cash equivalents, of which US$33.7 million was in the Debt Service Retention Account which is restricted pursuant to the Bond agreement. At the end of this month, the Bond will be amortized down to $202.5 million using funds already accrued in the DSRA.

John Rapach, Chief Operating Officer of Sterling, commented: "The recent hydraulic stimulation successes on Breagh wells A07 and A08 have led to RWE Dea and Sterling planning a more intensive further development of Phase 1 of the field with several more wells and possible side-tracks, all of which are expected to be hydraulically stimulated. The currently expected phasing of Breagh activity and the delay to Cladhan mean we have reduced our forecast production next year, but we expect higher production in 2016 and 2017 when we will benefit from the additional production from new wells, likely side-tracks and stimulations of some existing wells and the commencement of onshore compression on Breagh, coupled with our increased production from Cladhan."

Jake Ulrich, Chief Executive Officer of Sterling, added: "While we face continuing cash flow tightness in 2015, our portfolio should be delivering strong levels of operating cash flow in 2016-17 and beyond which we expect will facilitate a successful refinancing of our Bond. Our calculations show the remaining four wells and side-tracks for Breagh Phase 1 to have highly attractive economics, with cash payback in just over one year. In Romania, we have recently launched our equity reduction process with the benefit of new 3D seismic and we are very pleased with the strong level of industry interest. We are confident that the Romanian sell-down process will lead to a more appropriate balancing of our portfolio as well as some upfront cash. As well as the Romanian sell-down process and current financing activities, we continue to explore various asset and corporate transactions that would lead to an improvement in liquidity and accelerate our goal of delivering value for shareholders."