Drilling & Completions | Deals - Acquisition, Mergers, Divestitures | Hedging | Capital Markets | Capital Expenditure | Capex Increase | Capital Expenditure - 2022

PDC Updates Budget Following Great Western Deal; Adds $50MM

PDC Energy Inc. updated its 2022 guidance after closing the Great Western Petroleum acquisition earlier this month along with its updated multi-year outlook.

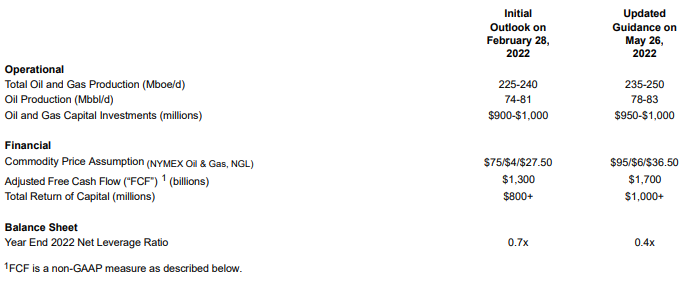

2022 Guidance Update

The Company's 2022 projected free cash flow yield is estimated at 25% based on our recent market capitalization. Our expected $1+ billion in total shareholder returns includes our increased base quarterly dividend of $0.35 per share, our share buyback program and expected year-end special dividend, all of which reflects a shareholder return yield of approximately 15% based on the Company's recent market capitalization.

President and Chief Executive Officer Bart Brookman commented, "We are excited to roll out our updated 2022 budget, which not only delivers top tier FCF generation of $1.7 billion each of the next two years, but also allows us outstanding shareholder returns of at least $1 billion annually. In the face of significant inflation, our operating teams have done a tremendous job innovating, driving additional efficiencies, and ensuring our capital budget remains at or below $1 billion. As we streamline our operations, the Great Western acquisition provides the Company with additional scale and high value inventory with increased shareholder returns. I want to thank the PDC team for their efforts to efficiently integrate operations according to plan and welcome all the new employees who have joined PDC."

2022 Operations Update

As previously announced, the Company closed on its core Wattenberg acquisition, Great Western, on May 6, 2022 and the guidance incorporates the effects of the transaction.

In the Wattenberg Field, the Company expects to invest $775-$825 million for 2022 to run a three rig program and one full time plus an intermittent completion crew. The drilling and completion activity will be conducted primarily on the Summit, Kersey and the newly acquired Great Western Range acreage. PDC expects to spud and complete 150 to 175 wells in 2022. The capital budget also includes non-op, infrastructure, land and ESG related projects.

The Company's Kenosha Oil and Gas Development Plan ("OGDP") is on the June 8th COGCC docket for anticipated approval. The Company's Broe OGDP has a preliminary hearing date of June 29, 2022. Combined, these two anticipated approvals will provide the Company an additional 100 permits for its 2024 drilling and completion plan. The Company continues to work with the COGCC on comments it received on its Guanella Comprehensive Area Plan. The Company intends to address and submit updated plans through June, which could put it on track for completeness determination in the third quarter.

In the Delaware Basin, the Company recently finished its 2022 completion program and is running one full time drilling rig. Capital expenditures are expected to total approximately $175 million for 16 spuds and 20 completions. The Company continues to be encouraged with its 2022 turn in line ("TIL") program as results from its relaxed spacing are outperforming expectations. On the Old Monarch pad, the Company TILed three U-Laterals (XRL equivalents) and three SRLs. With approximately three months of production history, the U-laterals are trending at or above a 1.5 MMboe Estimated Ultimate Recovery ("EUR") and the SRLs to a 0.7 MMBoe EUR. These wells were drilled on an 8-10 well per section equivalent spacing in the Wolfcamp A and B, where a U-lateral utilizes two lateral spaces. The Company expects to add additional U-shaped lateral locations to its inventory where appropriate.

2022 Capital Investment and Financial Guidance

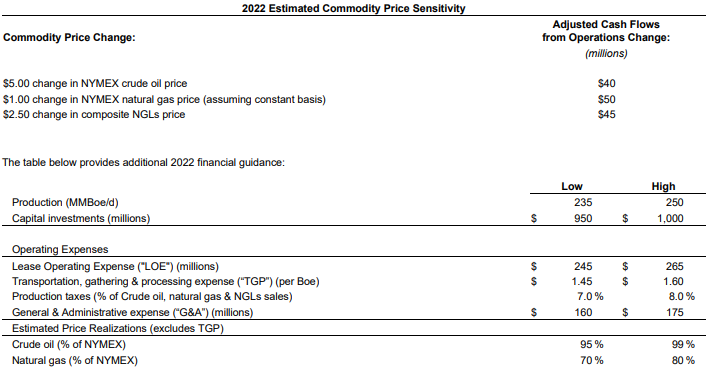

PDC anticipates 2022 capital investments of $950 to $1,000 million to generate between 235,000 and 250,000 Boe per day and 78,000 to 83,000 Bbls per day, after incorporating the Great Western capital and volumes beginning in May. The Company's updated guidance has been raised on the high side based on year to date performance and timing of the Great Western closing. The Company expects to produce on average 255,000 to 265,000 Boe per day for May through December 2022.

PDC expects this year's capital program to generate $1.7 billion of FCF, assuming $95 per Bbl WTI, $6.00 per Mcf NYMEX natural gas and NGL realizations of $36.50 per Bbl. As part of its strategy to methodically layer in hedges over time, the Company has hedges in place for approximately 60% oil and 40% natural gas of its remaining 2022 production (including those acquired in the Great Western acquisition).

Hedges for 2022 are as follows:

General and Administrative expense includes $20 to $25 million related to transaction and transition costs for the Great Western acquisition, which are not expected to be recurring.

At this time, the Company expects that for 2022 all Federal income tax expense will be deferred and that it will not be a cash taxpayer based on the commodity price outlook outlined above. In 2023, the Company expects that approximately one third of its Federal income tax would be deferred at the commodity price outlook.

The Company's second quarter outlook remains generally unchanged as it expects to invest nearly $260 -$290 million in the second quarter of 2022 and deliver total production and oil production of 240,000-250,000 Boe per day and 79,000-83,000 Bbls per day, respectively.

Multi-Year Outlook and Return of Capital Initiatives

The Company's outlook through 2023 is predicated on generating substantial levels of FCF through consistent capital investments from efficient operations with an output of low-single digit compound annual growth rate in both total production and oil production. With the 2022 pricing assumptions described above and assuming $85 per Bbl WTI, $5.00 per Mcf NYMEX natural gas and $31.50 NGL realizations in 2023, PDC projects to generate more than $1.7 billion of FCF in each of the next two years, which would bring the total two year cumulative FCF to $3.5 billion. Under the same price assumptions, PDC projects to reinvest less than 40 percent of its adjusted cash flows from operations in the development of crude oil and natural gas.

The Company recently announced its shareholder return framework in which at least 60% of FCF after base dividends will be returned to shareholders in the form of share repurchases and, if necessary, a year end special dividend. The Company has a $1.25 billion Board authorized share repurchase plan that it expects to fully utilize by the end of 2023. On May 26th, the Company's' board of directors approved a raised base quarterly dividend of $0.35 per share. The second quarter dividend is payable on June 23, 2022 to stockholders of record at the close of business on June 9, 2022. Based on our current estimated FCF and assuming we reach our annual $625 million share buyback goal, we anticipate that our year end special dividend could exceed $300 million.

PDC is committed to keeping a strong balance sheet as it executes on its capital return initiatives. Long term net debt is currently approximately $1.7 billion, representing a 0.7x pro forma net leverage ratio. The long term debt consists of $950 million of senior notes due in 2024 and 2026 with the balance drawn under its $1.5 billion revolving credit facility. The Company will repay borrowings under the revolving credit facility with the FCF generated and expects to have long term debt to be below $1.3 billion, which is a net leverage ratio of 0.4x, by year end 2022.

Environmental, Social and Governance Highlights

The Company's Board recently approved quantitative metrics for greenhouse gas ("GHG") and methane emissions reductions for its 2022 short term incentive program, including 15% GHG and 30% methane emissions reduction targets from 2021 to 2022, respectively. This supports the Company's previously announced goals to reduce by 2025 (from 2020 baseline levels and on a per unit of production basis) GHG and methane emissions by 60% and 50% respectively. In total, over 25% of the Company's short term incentive program is tied to ESG and EHS initiatives.

Related Categories :

Capex Increase

More Capex Increase News

-

Capex Plans Jump After 2Q: Nearly 30 E&P Companies Raise 2022 Budgets -

-

Riley Exploration Permian Second Quarter 2022 Results; Ups 2022 Capex

-

California Resources Second Quarter 2022 Results

-

Murphy Oil Second Quarter 2022 Results

-

Northern Oil Second Quarter 2022 Results

Permian News >>>

-

Seventeen (17) E&Ps; To Use 47 Frac Crews To Complete 2,800 Wells In 2024

-

These Permian Operators Plan to Complete/Frac 2,100 Wells IN 2024

-

Large E&P Chops Permian/Anadarko Basin Frac Activity by 30% In 2024

-

Permian E&P Ups 2024 Well Completed by +27% vs. 2023

-

Contrary to The Noise, U.S. Oil Production will Likely Growth 4-5% In 2024; A look Inside -