Dallas Fed Energy Survey: What Oil and Gas Executives Are Really Saying

The latest Dallas Fed Energy Survey shows a U.S. oil and gas industry that is not collapsing—but is clearly constrained. Executives are operating in a defensive posture, focused on protecting returns rather than pursuing growth, as uncertainty around prices, policy, and geopolitics remains elevated.

Activity and outlook: subdued, not broken

Survey respondents reported business activity that remains slightly negative, indicating that overall conditions are soft but stable. Company outlook sentiment is still pessimistic, though marginally improved from the prior quarter. The most telling metric remains uncertainty, which continues to register at historically high levels. Executives consistently cited policy unpredictability and geopolitical risk as key reasons for delaying capital commitments.

The takeaway is not fear, but hesitation. Companies are unwilling to commit incremental capital without greater confidence in price stability and regulatory clarity.

Production: flat by design

Oil production expectations remain slightly negative, while natural gas production expectations are essentially flat. This suggests operators are intentionally holding output steady rather than responding aggressively to short-term price movements.

Executives appear committed to maintenance mode—keeping production flat through efficiency gains rather than through additional rigs or frac crews. Growth is viewed as optional, not mandatory.

Capital spending: a ceiling has formed

Looking ahead to next year, responses show a wide dispersion in capital spending plans. Roughly equal portions of respondents expect spending to increase or decrease, while about a quarter expect budgets to remain flat.

Large E&Ps skew toward flat spending, signaling discipline and return protection. Oilfield services companies are more pessimistic, with nearly half expecting customer spending to decline. Smaller E&Ps show the widest range of outcomes, reflecting varying balance sheet strength and inventory quality.

Collectively, the data point to a capex ceiling: most companies are budgeting to defend cash flow, not to expand volumes.

Planning assumptions: $60 oil is the new anchor

One of the most important signals in the survey is the price deck executives are using for internal planning. The average planning assumption for WTI crude is around $59–60 per barrel—materially lower than last year’s budget assumptions.

When companies plan at $60 oil, several behaviors follow:

-

Fewer marginal or experimental wells

-

Higher hurdle rates for new projects

-

Increased emphasis on hedging

-

Greater openness to asset sales or consolidation

This planning mindset reinforces capital discipline even if spot prices temporarily rise.

Labor and costs: easing, but not reversing

Employment indicators weakened during the quarter, with fewer hours worked and reduced hiring momentum. However, forward-looking expectations suggest most companies plan to hold headcount steady rather than pursue broad layoffs.

Cost pressures are moderating, particularly in drilling and completion costs, but they remain directionally positive. Lease operating expenses continue to rise, reinforcing operator sensitivity to downside price risk.

Executives are not seeing cost deflation—only slower inflation—which limits operating leverage at lower prices.

Oilfield services: where the stress is showing

Service companies reported declining equipment utilization, negative pricing power, and sharply compressed margins. Operators are holding the line on activity and pushing back on service pricing, creating a classic late-cycle squeeze for the service sector.

This dynamic suggests that any further slowdown in E&P activity would disproportionately impact service providers before operators themselves materially cut production.

Commodity outlook: cautious realism

Survey participants expect oil prices to be modestly higher by the end of next year, but not high enough to justify a return to growth spending. Natural gas expectations are more mixed: while long-term demand from LNG exports, power generation, and data centers is viewed favorably, near-term operational realities—basis blowouts, contracts, and infrastructure constraints—are creating real pain.

Several respondents noted that gas has effectively become a cost in certain scenarios, rather than a revenue stream.

Qualitative intelligence: the real signal

The written comments provide the clearest insight into executive thinking:

-

Some operators warned that sustained lower oil prices could render portions of their inventory uneconomic.

-

Policy and geopolitical uncertainty are causing planning paralysis rather than outright cuts.

-

Gas is viewed as strategically attractive long term but operationally difficult in the near term.

-

Artificial intelligence is seen as a scale advantage for large operators, not a universal productivity breakthrough.

-

Smaller E&Ps are more willing to pivot toward gassier wells if economics improve.

Bottom line

The industry is operating with discipline, not optimism. Executives are managing toward durability at $60 oil, not upside at $80. Growth is optional, balance sheet strength is paramount, and uncertainty remains the dominant constraint on capital allocation.

This is an industry waiting—not retreating.

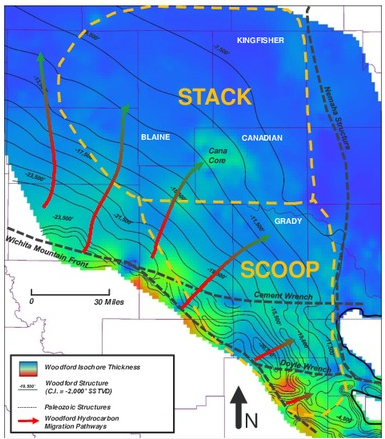

STACK News

-

-

ConocoPhillips to divest Anadarko Basin asset for $1.3B

August 10,2025| -

-

2025 Forecast : Dangerous Time Ahead

January 09,2025| -

Permian Basin News

-

Why $90 Oil Isn’t Bringing Back the Rigs

April 16,2026| -

-

-

-

Apa Corp : Doing More With Less

March 02,2026|