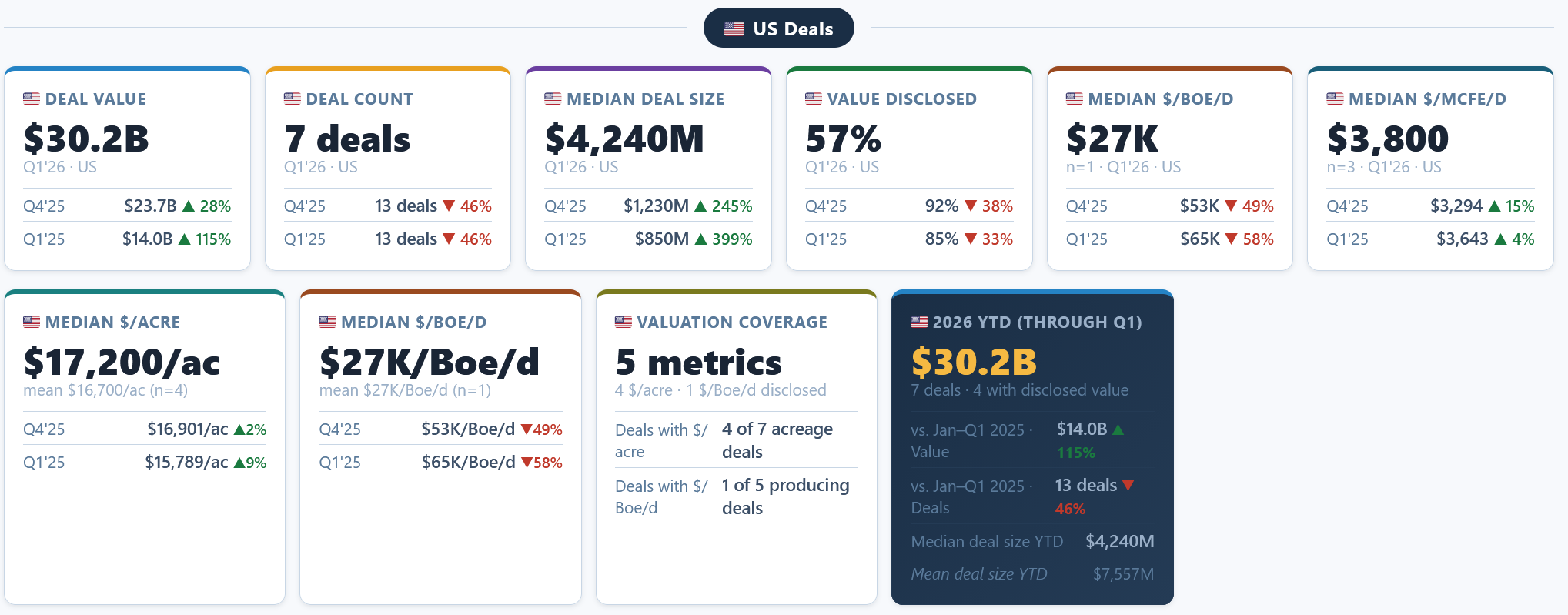

Q1 A&D Transactions Jump to $30B , While Deal Flow Was Down 40%

The first quarter of 2026 has officially defined the "Barbell Era" of American oil and gas. While the total number of deals plummeted by 46% YoY (dropping to just 7 major transactions), the total deal value skyrocketed to $30.2 Billion. The message from the market is clear: public E&Ps are no longer "shopping"—they are executing high-conviction, massive-scale mergers to secure the next decade of inventory.

The narrative this quarter was dominated by two structural shifts:

- The "Power Play" Era: The Devon/Coterra merger ($21.5B) proves that the market's biggest players are no longer content with being "Permian Pure-Plays." There is a rush to gain exposure to the Marcellus as AI data centers drive an unprecedented long-term demand for natural gas. Consolidation of two majors; $21.5B represents the transaction value, creating a $52B Pro Forma Enterprise Value giant.

- Global Capital Inflow: Mitsubishi’s $7.5B entry into the Haynesville signifies that US shale is now a critical link in the global LNG supply chain, with Japanese trading houses valuing long-term energy security over short-term yields.

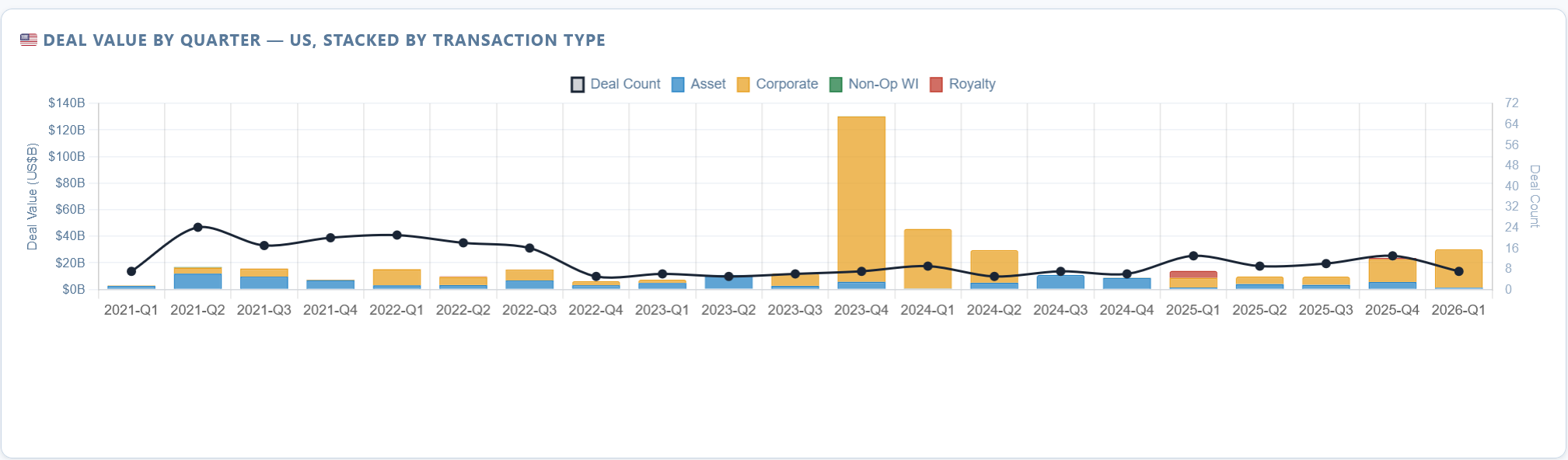

Section 1: Deal Volume & Value

Methodology Note: To maintain historical parity in our Deal Volume charts, we utilize the declared Transaction Value ($21.5B) for the Devon/Coterra merger. However, subscribers should note the combined entity’s Pro Forma Enterprise Value (TEV) of $52B, which underscores the massive scale of this 'Power Play' integration.

The Insight: The charts show a "Liquidity Trap" in the middle market.

- Total Deal Value: $30.2B (Highest Q1 in recent history).

- Total Deal Count: 7 (A record low).

- Commentary: There is a total absence of "Mid-Cap" consolidation. It’s either "Mega-Mergers" or "Small Bolt-ons." This suggests that private operators are holding out for higher valuations, while public companies are only willing to pay premiums for truly transformative, tier-one inventory.

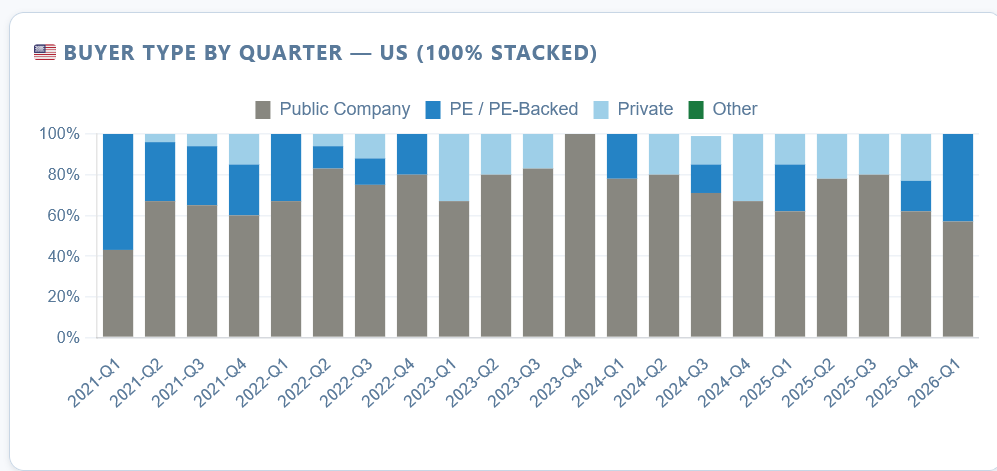

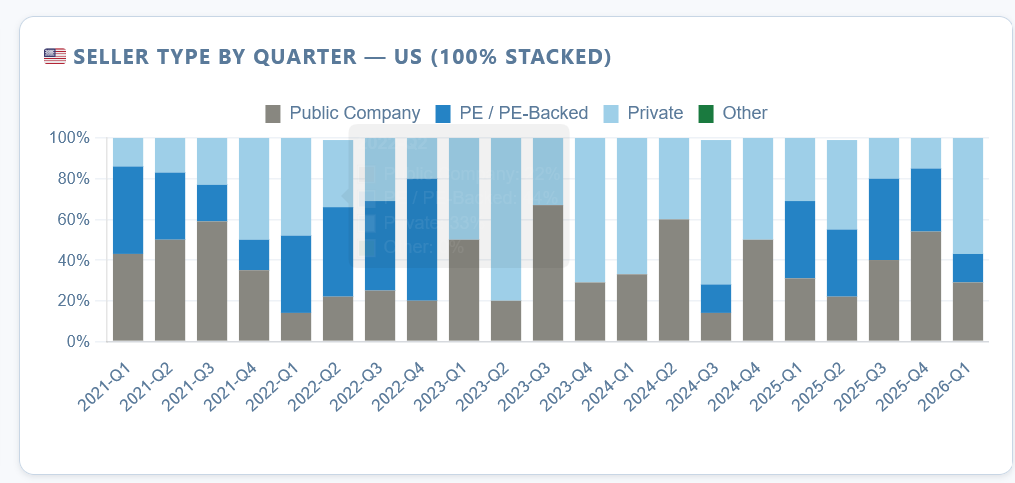

Section 2: Buyer & Seller Profiles (Stacked Chart Analysis)

Who is playing?

- Publics as Buyers: Represent roughly 85% of total capital spent. They are utilizing their stock at all-time highs as a cheap currency to acquire assets.

- PE as Sellers: PE-backed firms (Aethon, 1776 Energy) are in "Harvest Mode," capturing the valuation premiums created by the hunt for inventory.

- The Valuation Gap: We see a divergence in multiples. Gas assets are trading at a discount (3.5x - 4.2x), while "Oily" assets in the Eagle Ford and Delaware command premiums (5.0x+), as seen in the Caturus deal.

To understand the Q1 surge, one must look at the exit velocity of late 2025. The fourth quarter of 2025 was defined by a median multiple of 4.1x EBITDA, as buyers remained disciplined amid commodity volatility and a "wait-and-see" approach to federal drilling policies.

In contrast, Q1 2026 has seen a distinct multiple breakout for liquid-rich assets:

- The Divergence: While the Devon/Coterra merger held the line at a disciplined ~4.0x, the Caturus/SM Energy transaction at 5.9x Cash Flow signals that the market is now paying a ~40% premium for "Oily" inventory over "Gassy" corporate scale.

- The Shift: We have moved from the "Ground Game" bolt-ons of Q4 to high-conviction "Inventory Grabs." This 5.9x multiple represents the new "Scarcity Premium" being paid for Tier 1 acreage in basins where the remaining private inventory is rapidly disappearing.

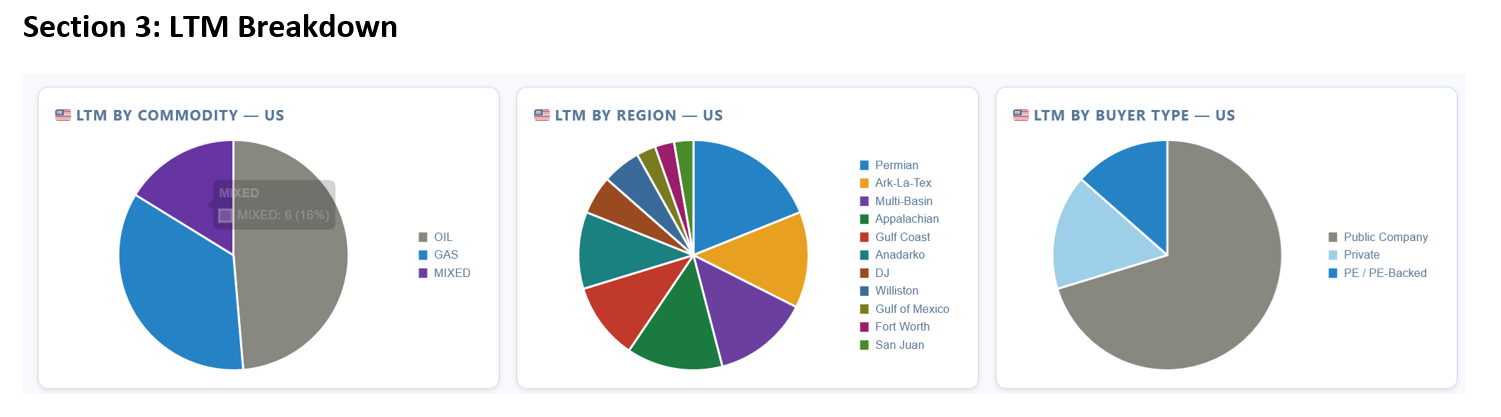

The Last 12 Months in Review:

- By Commodity: Natural gas has moved from 25% to 38% of total M&A focus over the last year. This is the "Data Center Effect"—buyers are looking for reliable gas feedstocks for domestic power.

- By Play: The Delaware Basin remains the "Home Base," but the Eagle Ford is seeing a resurgence as an "affordable alternative" to Permian prices, currently representing nearly 15% of the deal mix.

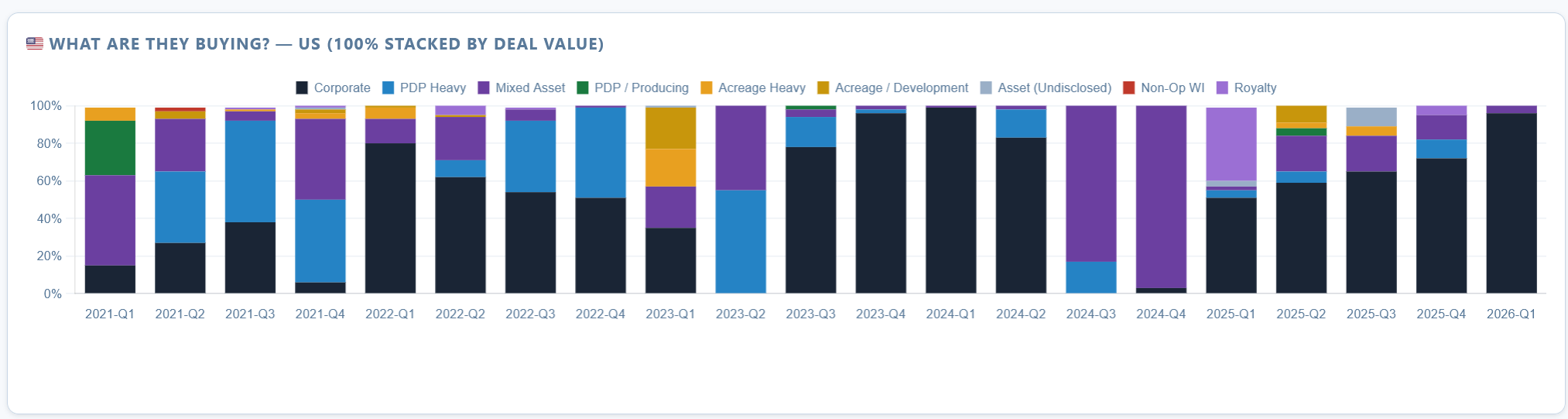

Section: What Are They Buying?

The Core Insight: The Return of the Corporate Mega-Deal Looking at the Q1 2026 data, Corporate deals represented nearly 95% of total deal value. This is a stark departure from previous years (like 2021 or 2023) where the market was balanced between "PDP Heavy" (buying existing production) and "Acreage/Development" (buying raw land).

1. "Corporate" is the New "Inventory" In a mature market, the easiest way to add 10+ years of drilling inventory is no longer through small acreage "bolt-ons," but by swallowing entire companies.

- The Trend: Buyers are prioritizing scale and synergy over individual asset characteristics.

- Evidence: The Devon/Coterra and Mitsubishi/Aethon transactions dominate this chart, showing that buyers are looking for integrated platforms that include infrastructure, midstream connectivity, and established teams—not just rocks in the ground.

2. The Disappearance of "PDP Heavy" and "Royalty" Plays For the first time in several quarters, we see almost zero activity in the "Royalty" or "Non-Op" sectors.

- The Logic: With public equity valuations at multi-year highs, companies are incentivized to do large, accretive corporate mergers. The "small ball" game of buying non-operated working interests has taken a back seat as the majors fight for basin dominance.

3. "Mixed Asset" Scavenging The tiny sliver of "Mixed Asset" activity (represented by the Caturus/SM Energy and Diversified deals) shows that there is still a market for surgical acquisitions.

- The Strategy: These buyers are picking up the "non-core" pieces shed by larger companies during their own consolidation. It’s a secondary market of scavenging where buyers look for high-margin, oily windows that don't fit the "Mega-Major" corporate profile.

Q2 2026 Market Outlook

As we head into the second quarter, the industry is watching the "Big Three" for the next move:

- EOG & Occidental: With Oxy’s recent $9.7B sale of its chemical business (OxyChem) to Berkshire Hathaway, their balance sheet is now primed for a major upstream acquisition. Expect them to target Permian or Rockies inventory to offset recent production plateaus.

- The Gas-Power Convergence: We anticipate at least one major "Utility-E&P" partnership or merger. As hyperscalers (Amazon/Google) demand 24/7 carbon-free and gas-backed power, the A&D market will shift from buying "rocks" to buying "energy solutions."

- Inventory Scarcity: With the "easy" deals done, the remaining private inventory in the Delaware is now commanding a "scarcity premium." Look for operators to move "down-pipe" into the Anadarko or Western Eagle Ford to find value.

In Other Deals - Acquisition, Mergers, Divestitures news

STACK & SCOOP News

-

Why Surface-Only Inventory Predictions Are a Fool’s Errand

October 07,2025| -

ConocoPhillips to divest Anadarko Basin asset for $1.3B

August 10,2025| -

-

-

Halliburton Warns of Deepening U.S. Frac Slowdown

July 23,2025|

Permian Basin News

-

Why $90 Oil Isn’t Bringing Back the Rigs

April 16,2026| -

-

-

Apa Corp : Doing More With Less

March 02,2026| -

Permian Resources to Grow Production 6% in 2026

February 26,2026|