Western Canada Upstream M&A: Q1 2026 Transaction Report

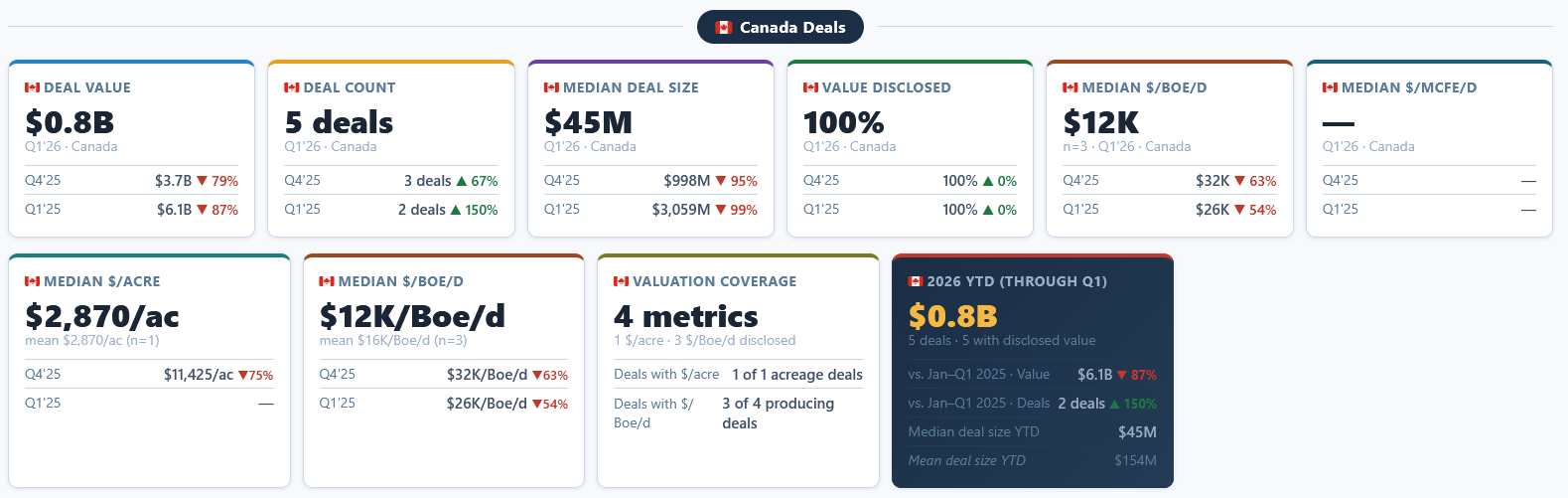

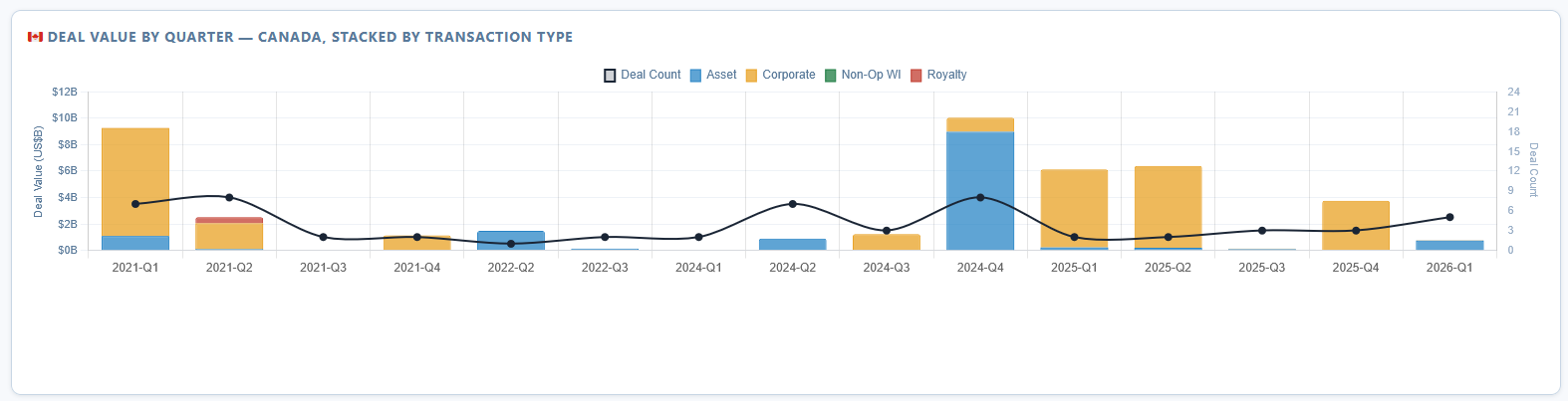

Western Canadian M&A activity in Q1 2026 was characterized by a 87% decrease in total deal value compared to Q1 2025, totaling $0.8 billion C$. However, transaction volume remained resilient with a 150% increase in deal count year-over-year. The quarter was defined by strategic high-grading by Majors and "bolt-on" consolidation by growth-oriented Juniors and Intermediates.

Market Dynamics & Valuation Benchmarks

1. Valuation Metrics

Activity was centered around producing assets (PDP) rather than undeveloped acreage.

-

Median Deal Size: $45 Million C$

-

Mean $/Boe/d: $16,000

-

Median $/Acre: $2,870

2. Basin & Play Analysis

-

Peace River High (PRH): The largest capital deployment of the quarter occurred here via CNRL’s acquisition of Tourmaline’s assets. The deal spans the Charlie Lake, Montney, and Wapiti Cardium plays, marking a significant infrastructure and production anchor for CNRL in the region.

-

Deep Basin / Montney: The Montney continues to be the primary engine for M&A. Logan Energy achieved 100% working interest at Simonette, while ARC Resources consolidated condensate-heavy acreage in Kakwa.

-

Heavy Oil: Activity remained niche but strategic, with Lycos Energy expanding its WCSB heavy oil footprint through a business combination with Mahikan.

3. Buyer & Seller Composition

-

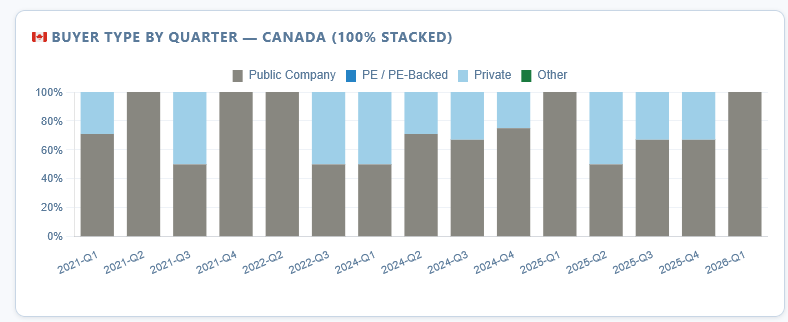

Buyer Profile: 100% of the active buyers were Public Companies, utilizing equity offerings and expanded credit facilities to fund acquisitions.

-

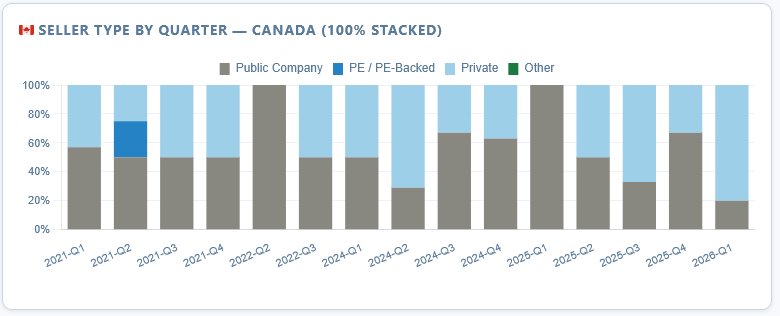

Seller Profile: Roughly 80% of sellers were Private companies, while the remaining 20% were Public Majors (like Tourmaline and Gran Tierra) divesting non-core "tail" assets to high-grade their portfolios.

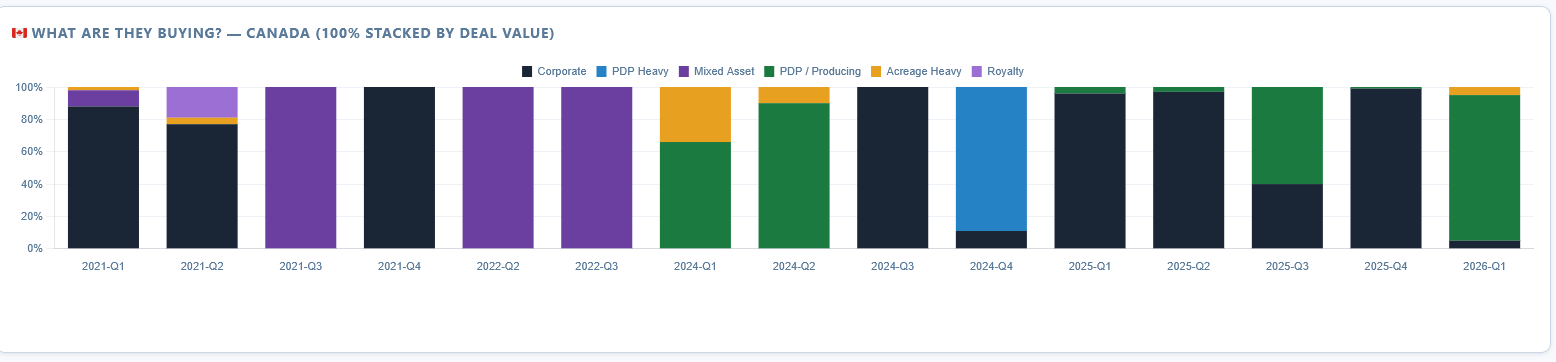

What are they buying

The trend for 2026 is focused on PDP-heavy, cash-flow positive assets that offer immediate accretion. While total capital deployment is lower than the massive corporate mergers of 2025, the increased deal count suggests a healthy environment for mid-tier consolidation and asset rotation.

In Other Deals - Acquisition, Mergers, Divestitures news

Duvernay Shale News

-

Whitecap Details 2026 Duvernay & Montney Program

December 23,2025| -

Paramount Targets 42% Higher 2026 Capex, More Duvernay Wells

December 02,2025| -

Baytex Energy Corp. First Quarter 2023 Results

May 08,2023| -

-

Murphy Oil Third Quarter 2022 Results

November 03,2022|

Montney Shale News

-

Whitecap Details 2026 Duvernay & Montney Program

December 23,2025| -

ARC Resources: Lower 2026 Capex, Higher Volumes

December 22,2025| -

Baytex 2026 Development Plans

December 18,2025| -

Tourmaline: 2026 Capital Program Locked In at $2.9B

December 18,2025| -

Advantage Plans $300–$330MM 2026 Capital Program

December 09,2025|