Quarterly / Earnings Reports | Fourth Quarter (4Q) Update | Financial Results | Capital Markets | Capital Expenditure | Drilling Program - Wells | Capital Expenditure - 2021

Diamondback Accelerating Completions 32% for 2021; Capex Set at $1.45B

Diamondback Energy, Inc. reported its 2021 capital plan as well as its Q4/full year 2020 results.

2021 Plan

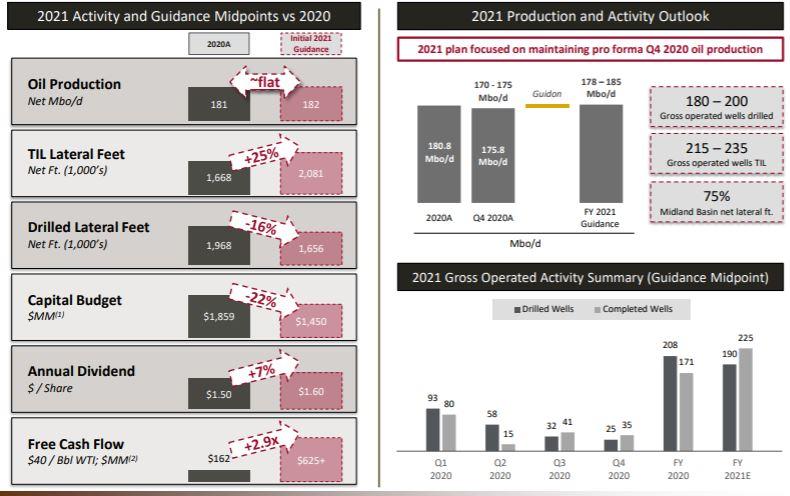

- Capex: $1.35-1.55 billion - down 22% at the midpoint from 2020 spending

- D,C&E: $1.07-1.21 billion

- Non-Op / Workovers: $150-170 million

- Midstream: $60-80 million

- Infrastructure / Environment: $70-90 million

- Wells Drilled: 180-200 gross wells (156-172 net) - down 9% at the midpoint from 2020

- Wells Completed: 215-235 gross wells (197-215 net) - up 32% at the midpoint from 2020

- Production: 308-325 MBOEPD

- Oil Production: 178-185 MBOPD - flat from 2020

Q4 / 2020 Results

Highlights:

- Q4 2020 average production of 175.8 MBO/d (299.0 MBOE/d), with average daily oil production up 3% over Q3 2020

- Generated Q4 2020 cash flow from operating activities of $403 million. Operating Cash Flow Before Working Capital Changes (as defined and reconciled below) of $468 million

- Q4 2020 cash capital expenditures of $226 million; Q4 2020 activity-based capital expenditures incurred of approximately $200 million

- Generated Q4 2020 Free Cash Flow (as defined and reconciled below) of $242 million

- Q4 2020 cash operating costs of $6.87 per BOE; including cash general and administrative ("G&A") expenses of $0.51 per BOE and lease operating expenses ("LOE") of $3.38 per BOE

- Increasing annual dividend by 6.7% to $1.60 per share; declared Q4 2020 cash dividend of $0.40 per share payable on March 11, 2021; implies a 2.4% annualized yield based on the February 19, 2021 share closing price of $65.57

- Flared 0.9% of gross natural gas production in the fourth quarter. For the full year ended 2020, flared 2.0% of gross production, down 64% year over year

- Received $103 million federal net operating loss carryback and alternative minimum tax credit refund subsequent to quarter end in January 2021, which included $3 million of interest income

- Announced pending all-stock acquisition of QEP Resources ("QEP") and acquisition of all leasehold interests and related assets of Guidon Operating LLC ("Guidon"). Guidon acquisition is expected to close on Friday, February 26, 2021. QEP stockholder meeting is scheduled for March 16, 2021 to vote on the pending merger. The merger is expected to close shortly thereafter subject to QEP stockholder approval.

- Full year 2020 average production of 180.8 MBO/d (300.3 MBOE/d)

- Generated full year 2020 cash flow from operating activities of $2.1 billion. Operating Cash Flow Before Working Capital Changes (as defined and reconciled below) of $2.0 billion

- Full year 2020 cash capital expenditures of $1.86 billion; full year 2020 activity-based capital expenditures incurred of approximately $1.40 billion; turned 171 operated horizontal wells to production

- Generated full year 2020 Free Cash Flow of $162 million despite dramatic drop in commodity prices

- Proved reserves as of December 31, 2020 of 1,316 MMBOE (759 MMBo, 58% oil), up 17% year over year; proved developed producing ("PDP") reserves of 817 MMBOE (443 MMBo, 54% oil, 62% of proved reserves), up 8% year over year

- 2020 consolidated proved developed finding and development ("PD F&D") costs of $9.65/BOE; drill bit finding and development costs of $5.00/BOE

CEO Travis Stice said: "Diamondback executed flawlessly in the fourth quarter of 2020, setting the Company up well for continued solid operational performance in 2021. The benefits of the Company's strategy to move activity to our most productive areas is now starting to pay dividends in terms of capital efficiency and early-time well performance. While the impact of the recent winter storms in the Permian Basin will be significant for first quarter production, we expect to overcome this adversity for the full year 2021 and I am proud of how our field organization responded to this challenge. Well costs and cash operating costs remain near all-time lows, which provide for increased returns to our stockholders as commodity prices have risen in recent months.

Mr. Stice continued, "We are still operating in a market supported by supply that is being purposely withheld to allow global inventories to decline as demand recovers from the depths of the global pandemic. Diamondback continues to see no need to grow oil production into this artificially undersupplied market, and instead plans to hold fourth quarter 2020 production flat while generating Free Cash Flow used to pay our dividend and pay down debt. The Board's decision to increase the dividend today exhibits its confidence in the forward development plan released today, which further demonstrates our commitment to capital discipline. We look forward to closing and successfully integrating the Guidon assets and the pending QEP merger, and will be prepared to update the market on our pro-forma plan as soon as practicable. As I have mentioned previously, using Free Cash Flow to pay down debt does not preclude Diamondback from increasing cash returns to stockholders."

Dividend

Diamondback announced today that the Company's Board of Directors approved a 6.7% increase to the Company's annual dividend to $1.60 per share from $1.50 previously and declared a cash dividend of $0.40 per common share for the fourth quarter of 2020 payable on March 11, 2021, to stockholders of record at the close of business on March 4, 2021. Future dividends remain subject to review and approval at the discretion of the Company's Board of Directors.

Environmental Strategy Update

Diamondback today announced significant changes to its environmental, social and governance ("ESG") performance and disclosure, including Scope 1 and methane emissions intensity reduction targets as well as a commitment to point forward Scope 1 carbon neutrality, or "Net Zero Now." The Company plans to update investors on its progress on the below initiatives in both quarterly reporting as well as in its annual Corporate Responsibility Report, which is traditionally published in the third quarter.

- Greenhouse Gas (GHG) Emissions Intensity Reduction Targets

Diamondback is committing to reduce its Scope 1 GHG intensity by at least 50% from 2019 levels by 2024

Diamondback is committing to reduce its methane intensity by at least 70% from 2019 levels by 2024

More detail on the breakdown of and plan to reduce Diamondback's current emissions can be found in the Company's investor presentation posted to its website - "Net Zero Now"

Diamondback today announced the "Net Zero Now" initiative, which means that as of January 1, 2021, every hydrocarbon molecule produced by Diamondback is anticipated to be produced with zero net Scope 1 emissions

The GHG and methane intensity reduction targets announced today are the primary focus of the Company as it relates to environmental responsibility, and the Company recognizes it will still have a carbon footprint. Therefore, carbon offset credits will be purchased to offset the remaining emissions

Should the Company exceed its GHG reduction targets, then less carbon offset credits will need to be purchased, incentivizing the Company to continue to reduce its Scope 1 carbon footprint

The Company, or one of its subsidiaries, intends to eventually invest in income-generating projects that will more directly offset its remaining Scope 1 emissions - Plan to increase the weighting of ESG metrics in the Company's 2021 annual short-term incentive ("STI") plan to a weighting of 20% from 15% previously

ESG Component to be determined by meeting or exceeding the same key environmental and safety metrics as 2020: flaring intensity, GHG intensity, recycled water percentage, fluid spill control and Total Recordable Incident Rate (safety)

Each metric will be measured and compensation will be tied to the metrics presented

Thresholds will all meet or exceed 2020 actual performance

"With these major announcements today, Diamondback has chosen to adopt a strategy to operate with the highest level of environmental responsibility. We have been encouraged by our stockholders to embrace and lead this transition, irrespective of regulatory, political or social pressures. Gas operators have traditionally operated with a low carbon footprint, and we believe it is time for oil-focused operators to follow the example they have set, albeit with different emissions limitations inherent in oil production. Our social and environmental license to operate as a public oil and gas company based in the United States is going to be influenced by our capital providers, and we do not expect investor pressure for oil and gas companies to improve their environmental performance to subside. It is incumbent on us to improve our environmental performance and compete for capital in an industry with ever-increasing external pressures. Carbon emissions are a cost, and Diamondback is working to become the low-carbon operator in addition to our leadership position as the operator with the lowest capital and operating costs," stated Travis Stice, Chief Executive Officer of Diamondback.

Mr. Stice continued, "The energy transition is here and oil and gas are commodities that will play a vital role in fueling this transition and global growth for decades, regardless of public policy or perception. But, our industry must acknowledge this reality, and change behaviors in order to succeed in this new energy economy. With these announcements today, Diamondback is choosing to implement this new strategy because we think it is the right thing to do for the long-term benefit of our stockholders' investment."

Governance & Compensation Update

Additionally, Diamondback today announced changes to its compensation program. The Company plans to provide additional detail for these and other changes in its upcoming proxy, which it expects to file in the second quarter of 2021.

- Chief Executive Officer's Long Term Incentive ("LTI") compensation target amount reduced by 20% from 2020

- Remainder of executive team 2021 LTI compensation target amount reduced by 10% from 2020

- No upward salary adjustments or change to STI targets for all members of the executive team

- 2020 STI scorecard performance to be capped at 100% of target for all executives despite actual scorecard performance of approximately 160% of target

- Plan to update annual STI scorecard metrics to include a Free Cash Flow per share metric with expected weighting of 20% and increase weighting of current ESG metric to 20% as previously mentioned

2021 scorecard metrics expected to include: Capital costs per lateral foot, PDP F&D costs, controllable cash costs including LOE and G&A, Return on Average Capital Employed, Free Cash Flow per Share and quantitative ESG metrics - Both the S&P 500 and the XOP Index have been added as peers to the 2021 peer group

"Diamondback continues to respond to investor feedback and make appropriate changes to compensation and governance practices to reflect incentives that translate to stockholder value creation. The Company has not had a production or reserves growth metric in its scorecard since 2014, added a return on average capital employed metric in 2018, and added specific, measurable ESG metrics in 2020. This year, the Company is adding a Free Cash Flow per share metric to the scorecard. Financial metrics are now expected to make up 40% of the scorecard, with operational metrics expected to make up another 40% and environmental and safety performance expected to make up the remaining 20%. As mentioned previously, one unique aspect of Diamondback's annual cash incentive program is that while 100% of senior management's cash incentive compensation is tied to the scorecard, half of each employee's discretionary cash incentive compensation is also tied to the same scorecard, creating alignment throughout the organization," stated Steve West, Chairman of the Board of Directors of Diamondback.

Ops Update

The tables below provide a summary of operational activity for the fourth quarter of 2020.

| Total Activity (Gross Operated): | |||||

| Area | Number of Wells Drilled | Number of Wells Completed |

|||

| Midland Basin | 19 | 24 | |||

| Delaware Basin | 6 | 11 | |||

| Total | 25 | 35 | |||

| Total Activity (Net Operated): | |||||

| Area | Number of Wells Drilled | Number of Wells Completed |

|||

| Midland Basin | 17 | 24 | |||

| Delaware Basin | 5 | 11 | |||

| Total | 22 | 35 | |||

During the fourth quarter of 2020, Diamondback drilled 19 gross horizontal wells in the Midland Basin and six gross horizontal wells in the Delaware Basin. The Company turned 24 operated horizontal wells to production in the Midland Basin and 11 operated horizontal wells to production in the Delaware Basin. The average lateral length for the wells completed during the fourth quarter was 13,034 feet. Operated completions during the fourth quarter consisted of 20 Wolfcamp A wells, eight Lower Spraberry wells, five Wolfcamp B wells, one Jo Mill well and one Third Bone Spring well.

For the full year ended December 31, 2020, the Company drilled 208 gross horizontal wells and turned 171 operated horizontal wells to production. The average lateral length for wells completed during the year ended 2020 was 10,585 feet, and consisted of 87 Wolfcamp A wells, 25 Lower Spraberry wells, 21 Wolfcamp B wells, 17 Middle Spraberry wells, 11 Second Bone Spring wells, six Third Bone Spring wells and four Jo Mill wells.

Financials

Diamondback's fourth quarter 2020 net loss was $739 million, or $4.68 per diluted share. Adjusted net income (a non-GAAP financial measure as defined and reconciled below) was $130 million, or $0.82 per diluted share. Fourth quarter 2020 net loss includes a non-cash impairment charge of $1,022 million as a result of the lower SEC Pricing because of the sharp decline in commodity prices.

Fourth quarter 2020 Consolidated Adjusted EBITDA (as defined and reconciled below) was $528 million. Adjusted EBITDA net of non-controlling interest was $475 million.

Fourth quarter 2020 average unhedged realized prices were $38.64 per barrel of oil, $1.35 per Mcf of natural gas and $14.68 per barrel of natural gas liquids, resulting in a total equivalent unhedged price of $27.41 per BOE.

Diamondback's cash operating costs for the fourth quarter of 2020 were $6.87 per BOE, including LOE of $3.38 per BOE, cash G&A expenses of $0.51 per BOE, production and ad valorem taxes of $1.71 per BOE and gathering and transportation expenses of $1.27 per BOE.

As of December 31, 2020, Diamondback had $61 million in standalone cash and $23 million of borrowings outstanding under its revolving credit facility, with approximately $1.98 billion available for future borrowing under the facility and $2.04 billion of total liquidity.

During the fourth quarter of 2020, Diamondback spent $197 million on drilling and completion, $7 million on midstream, $12 million on infrastructure and $10 million on non-operated properties, for total capital cash expenditures of $226 million. For the year ended December 31, 2020, the Company spent $1.55 billion on drilling and completion, $140 million on midstream, $108 million on infrastructure and $58 million on non-operated properties, for total capital cash expenditures of $1.86 billion.

Reserves

Ryder Scott Company, L.P. prepared estimates of Diamondback's proved reserves as of December 31, 2020. Reference prices of $39.57 per barrel of oil and $1.99 per MMbtu of natural gas were used in accordance with applicable rules of the Securities and Exchange Commission. Realized prices with applicable differentials were $38.06 per barrel of oil, $0.09 per Mcf of natural gas and $10.83 per barrel of natural gas liquids.

Proved reserves at year-end 2020 of 1,316 MMBOE represent a 17% increase over year-end 2019 reserves. Proved developed reserves increased by 8% to 817 MMBOE (62% of total proved reserves) as of December 31, 2020, reflecting the continued development of the Company's horizontal well inventory. Proved undeveloped reserves ("PUD" or "PUDs") increased to 500 MMBOE, a 36% increase over year-end 2019, and are comprised of 666 locations, of which 149 are in the Delaware Basin. Crude oil represents 58% of Diamondback's total proved reserves.

Net proved reserve additions of 299 MMBOE resulted in a reserve replacement ratio of 272% (defined as the sum of extensions, discoveries, revisions, purchases and divestitures, divided by annual production). The organic reserve replacement ratio was 269% (defined as the sum of extensions, discoveries and revisions, divided by annual production).

Extensions and discoveries of reserves were the primary contributor to the increase in reserves totaling 302 MMBOE followed by net purchases of reserves totaling 3 MMBOE, with divestitures of 1 MMBOE and downward revisions of 6 MMBOE. PDP extensions accounted for 22% of the total increase in reserves. PDP extensions were the result of 129 wells in which the Company has a working interest, and PUD extensions were the result of 277 new locations in which the Company has a working interest. Net acquisitions of reserves of 3 MMBOE were the net result of acquisitions of 3.5 MMBOE and divestitures of 0.5 MMBOE. Downward revisions of 6.3 MMBOE were primarily the result of negative revisions due to lower commodity pricing of 54.6 MMBOE, which were partially offset by positive revisions of 23.1 MMBOE associated with a reduction in LOE, resulting in a total negative pricing revision of 31.6 MMBOE. Downgrades of 31.1 MMBOE were predominantly from changes in the corporate development plan. These revisions were offset by positive performance revisions of 56.4 MMBOE associated with less gas flaring and a corresponding increase in NGL recoveries. Downward revisions of 78.2 MMBO were primarily the result of negative revisions due to lower commodity pricing of 25.3 MMBO, which were partially offset by positive revisions of 11.6 MMBO associated with a reduction in LOE, resulting in total negative pricing revision of 13.7 MMBO. Downgrades of 19.6 MMBO were predominantly from changes in the corporate development plan. Of the negative 44.9 MMBO performance revisions, 35.7 MMBO were associated with changes to PDP estimates and 9.3 MMBO were associated with changes to PUD type curves.

Related Categories :

Capital Expenditure - 2021

More Capital Expenditure - 2021 News

-

Pine Cliff Energy Ups Spending, Production Plans by 10% for 2022

-

Whitecap Resources Unveils 2022 Budget; Up 12% vs. 2021

-

Southwestern Closes Acquisition of Indigo Natural Resources; Ups Capex

-

Altura Energy First Quarter 2021 Results

-

Razor Energy Corp. First Quarter 2021 Results

Permian News >>>

-

Why $90 Oil Isn’t Bringing Back the Rigs -

-

These Three Companies Will Increase Drilling & Completion Over The Next 3 Year -

-

Q1 A&D Transactions Jump to $30B , While Deal Flow Was Down 40%

-

Wright to U.S. Oil Industry: The Price Signal Is Telling You to Drill

-

Apa Corp : Doing More With Less