Drilling & Completions | Quarterly / Earnings Reports | Second Quarter (2Q) Update | Key Wells | Financial Results | Capital Markets | Capital Expenditure | Drilling Activity

EQT Corp. Second Quarter 2021 Results

EQT Corp. announced financial and operational results for the second quarter 2021.

Second Quarter and Other Highlights:

- Sales volumes of 421 Bcfe, in-line with guidance

- Total per unit operating costs of $1.33/Mcfe, in-line with annual guidance

- Capital expenditures of $246 MM, $19 MM below the low-end of guidance range

- Net cash provided by operating activities of $43 MM; free cash flow(1) of $155 MM

- Announced targets to achieve net zero Scope 1 & Scope 2 GHG emissions by or before 2025

- Successfully closed the acquisition of Alta Resources on July 21, 2021

- Received credit rating upgrade by Fitch Ratings in May 2021

- Upgraded by Moody's Investor Services and S&P Global in July 2021

President and CEO Toby Rice stated, "The closing of the Alta acquisition represents another important step forward in creating value for our stakeholders. These premier assets will accelerate our deleveraging strategy, provide attractive free cash flow accretion, and enhance strategic opportunities. We are excited to fully integrate these high-margin assets into EQT's already robust portfolio, while working alongside and building strong relationships with the new business partners established with the transaction. We are a values-driven organization designed to perform for our stakeholders, and we are eager to deliver the prolific value embedded in these assets."

Rice continued, "We have entered the sustainable shale era, which is driven by free cash flow generation, balance sheet strength, the pursuit of net zero emissions, and returning capital to shareholders. These concepts are firmly embedded in our multi-level strategy geared towards sustainable value creation. We continue to Evolve to realize the full potential of EQT's assets, diligently monitor the market in an effort to capture accretive Consolidation opportunities, and explore New Ventures in an effort to forge new paths and open new markets to achieve sustainable growth. We are executing this strategy with vision and purpose, as we continue on our path to become the clear operator of choice for all stakeholders."

Q2 Financials

Net loss attributable to EQT Corporation for the three months ended June 30, 2021 was $936 million, $3.35 per diluted share, compared to net loss attributable to EQT Corporation for the same period in 2020 of $263 million, $1.03 per diluted share. The change was attributable primarily to the loss on derivatives not designated as hedges and lower income from investments, partly offset by increased sales of natural gas, natural gas liquids (NGLs) and oil and a higher income tax benefit. For the three months ended June 30, 2021, the Company recognized a loss of $1.3 billion on derivatives not designated as hedges related primarily to decreases in the fair market value of the Company's NYMEX swaps and options due to increases in forward prices.

Sales volume increased compared to the same period in 2020 primarily as a result of prior period sales volume decreases of 36 Bcfe from the 2020 Strategic Production Curtailments (defined below) and sales volume increases of 33 Bcfe from the assets acquired from the Chevron Acquisition (defined below). The 2020 Strategic Production Curtailments refers to the Company's strategic decision to temporarily curtail approximately 1.4 Bcfe per day of gross production, equivalent to approximately 1.0 Bcfe per day of net production, beginning on May 16, 2020 and remaining shut in through the remainder of the second quarter of 2020. The Chevron Acquisition refers to the Company's acquisition of upstream assets from Chevron U.S.A. Inc. in the fourth quarter of 2020.

Net cash provided by operating activities decreased by $404 million due primarily to increased collateral and margin deposits associated with the Company's over the counter (OTC) derivative instrument contracts and exchange traded natural gas contracts. Free cash flow(1) increased by $237 million compared to the same quarter last year due primarily to increased revenues from higher sales volume and lower capital expenditures.

Gathering expense per Mcfe decreased when compared to the same period in 2020 due primarily to increased sales volume, which resulted in utilization of lower overrun rates as part of the Company's consolidated gas gathering and compression agreement with Equitrans Midstream Corporation (Equitrans Midstream), and a lower gathering rate structure on the assets acquired from the Chevron Acquisition. Transmission expense per Mcfe decreased when compared to the same period in 2020 due primarily to increased sales volume, some of which does not have associated transmission expense, such as the assets acquired from the Chevron Acquisition.

Liquidity

As of June 30, 2021, the Company had no credit facility borrowings and $0.7 billion letters of credit outstanding under its $2.5 billion credit facility. As of June 30, 2021, total debt was $5,496 million and net debt(1) was $5,166 million, compared to $4,925 million and $4,907 million, respectively, as of December 31, 2020.

As of July 27, 2021, the Company had sufficient unused borrowing capacity under its credit facility, net of letters of credit, to satisfy any collateral requests that its counterparties would be permitted to request of the Company pursuant to the Company's OTC derivative instruments, midstream services contracts and other contracts. As of July 27, 2021, such amounts could be up to approximately $1.2 billion, inclusive of letters of credit, OTC derivative instrument margin deposits and other collateral posted of approximately $1.2 billion in the aggregate.

Strategic Update

As previously announced, on July 16, 2021, the Company's shareholders overwhelmingly approved the issuance of EQT common stock as partial consideration for the acquisition of Alta Resources Development, LLC's (Alta) upstream and midstream assets (the Alta Acquisition). On July 21, 2021, the Company closed the Alta Acquisition for an adjusted aggregate purchase price consisting of $1.0 billion in cash and approximately 98.8 million shares of the Company's common stock being issued directly to Alta's equity holders or their designees.

As a result of the Alta Acquisition, the Company acquired approximately 300,000 net Northeast Marcellus acres, approximately 1.0 Bcfe per day of current net production, approximately 300 miles of midstream gathering systems, approximately 100 miles of a freshwater system and an attractive firm transportation portfolio to premium demand markets.

During the remainder of 2021, the Company anticipates capital expenditures of approximately $100-$125 million and sales volumes of approximately 155-175 Bcfe related to the Alta Acquisition. Additionally, the Company expects the assets acquired from the Alta Acquisition to contribute approximately $300-$325 million in adjusted EBITDA and $150-$170 million in free cash flow during 2021. On average, the Company expects to deploy one operated horizontal rig and frac crew on the acquired Alta assets during the remainder of 2021.

The Company is in the early stages of implementing its proven integration framework, which provides a comprehensive and transparent roadmap to fully assimilate all operational, technological and administration functions from the acquisition. This platform will drive seamless integration of the acquired assets, while quickly identifying enhancement opportunities as the assets are integrated. The Company anticipates being completed with all operational integration tasks by the end of 2021.

Operations Update

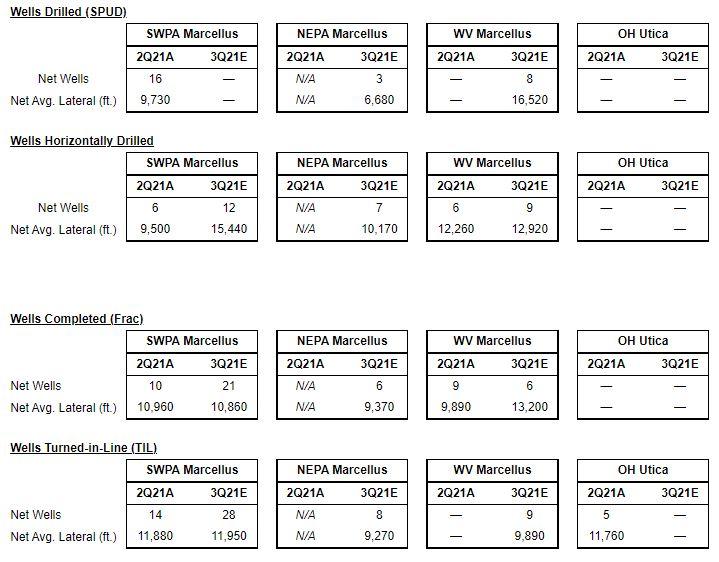

The Company continues to deliver operational results across the organization that meet or exceed expectations. During the second quarter 2021, the Company averaged approximately $710 per foot in the PA Marcellus, and when combined with the $635 per foot delivered in the first quarter 2021, the Company's year-to-date 2021 average is $670 per foot in the PA Marcellus. The increase in well cost per foot during the second quarter 2021 was solely driven by the lateral lengths associated with the set of wells developed during the period. The Company did not experience any operational issues, or service cost inflationary pressures during the period, and is on pace to meet or exceed its full-year PA Marcellus well cost target of $675 per foot.

In July 2021, the Company placed into service a 15-mile section of its planned 45-mile mixed-use water system, which will serve as the backbone for the optimal development of the Company's WV Marcellus assets. The completed section has the ability to deliver up to 100 barrels of water per minute to support completion activities and is expected to service over 100 wells in Wetzel and Marion County, WV. By partnering with the Company's service providers on cost savings initiatives and effective work planning, the completed section was delivered ahead of schedule and under budget. During 2021, development activity in the WV Marcellus has been executed as planned, and the Company has high confidence that it will meet or exceed its full-year 2021 well cost target of $775 per foot in the WV Marcellus. Moving forward, utilization of the water system is expected to enhance development efficiencies, while also reducing environmental impacts and improving long-term lease operating expenses.

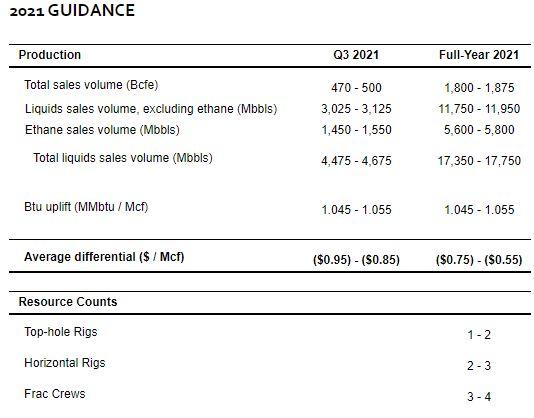

2021 Guidance

Related Categories :

Second Quarter (2Q) Update

More Second Quarter (2Q) Update News

-

Berry Reaffirms FY25 Guidance; Uinta Wells Drive 2H Growth

-

SM Energy Hits Record Output; Driven by Uinta

-

Expand Energy Talks, Wells, Frac Crews, Production For 2H-2025 -

-

Comstock Rides Higher Gas Prices, Operational Momentum in Q2 2025

-

A Quarter of Quiet Strength: CNX’s Patient Ascent in Appalachia -

Northeast News >>>

-

Why $90 Oil Isn’t Bringing Back the Rigs -

-

Q1 A&D Transactions Jump to $30B , While Deal Flow Was Down 40%

-

Ascent Resources 2026: A Quiet Growth Story for Oilfield Services

-

Infinity Closes $1.2B Utica Upstream & Midstream Deal

-

Antero Resources Completes $2.8B Marcellus Expansion

Northeast - Appalachia News >>>

-

A Quiet Capital Pattern Is Forming in North American Upstream — and Almost No One Is Talking About It -

-

Ascent is quietly setting the Utica productivity curve

-

Kimmeridge Offers $6 Billion for Ascent Resources: A Bid Lands in the Middle of a High-Stakes Sponsor Dispute

-

Dallas Fed Energy Survey: What Oil and Gas Executives Are Really Saying

-

Infinity and NOG Buy Antero's Ohio Utica Assets for $1.2B: A Vertical-Integration Utica Power Move