Capital Markets | Capital Expenditure | Credit Facility Change | Capital Expenditure - 2022

Crescent Point Energy Ups 2022 Capex 44% YOY to ~$900 Million

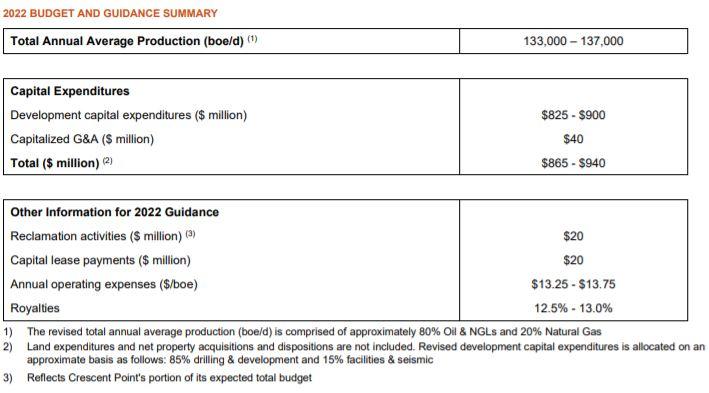

Crescent Point Energy Corp. has detailed its formal 2022 capital expenditures budget and production guidance, as well as shareholder return and divident information.

2022 Overview

- Capital Budget: $865 to $940 million ($825-900 million D&C capital) - up 44% from 2021 spending levels

- Kaybob Duvernay: $215-234 million (26%)

- Shaunavon: $157-171 million (19%)

- North Dakota Bakken: $149-162 million (18%)

- Viewfield Bakken: $132-144 million (16%)

- Flat Lake: $83-90 million (10%)

- Capitalized G&A: $40 million

- Production: 133,000 to 137,000 boe/d - up 2.3% vs. 2021 levels

The company cited expected 2022 excess cash flow of $750 million to $1.0 billion at US$65/bbl to US$75/bbl WTI, supported by a strong hedge book.

It also successfully renewed unsecured, covenant-based credit facilities totaling $2.3 billion and extended maturity to November 2025.

Craig Bryksa, President and CEO of Crescent Point, said: "We have established a disciplined budget for 2022 and expect to generate strong returns and significant excess cash flow for our shareholders. In the coming year, we plan to build on our track record of strong performance focused on our key pillars of balance sheet strength and sustainability. Through our discipline and execution, including recent successes in the Kaybob Duvernay, we continue to make significant progress toward meeting our debt targets. As a result, we are accelerating our plans to return additional capital to shareholders in the form of another dividend increase and share repurchases. As we continue to strengthen our balance sheet, we expect to further increase our return of capital offering to shareholders in the context of our capital allocation framework."

Kaybob Duvernay Update

During fourth quarter 2021, Crescent Point successfully concluded drilling its first multi-well pad in the Kaybob Duvernay, with completion operations currently underway. The Company also recently started drilling its second multi-well pad in the play, with completions expected in the first half of 2022.

Crescent Point's Kaybob Duvernay well costs, including drilling, completion, equip and tie-in, are now approximately $8.75 million. Current well costs are now down approximately $1.50 million, or 15 percent, from estimated costs when the Company originally entered the play in second quarter 2021. These initial savings, which include the previously announced completion cost reductions of approximately 20 percent, or $1.00 million per well, were realized despite using a larger frac design to increase recoverable reserves. The Company will continue to focus on cost improvements and enhancing overall returns with ongoing drilling and completions optimization.

Crescent Point expects to release production data for its initial wells, including partner wells completed as part of its recent farm-in agreement, in early 2022 after attaining 30-day rates. Those wells that are currently onstream, or awaiting tie-in, have demonstrated strong initial flowback results.

Crescent Point's strategic entry into the Kaybob Duvernay in 2021 has significantly enhanced the Company's balance sheet strength and sustainability. The Kaybob Duvernay represents the largest allocation by area within Crescent Point's 2022 budget at over 25 percent, given the play's competitive economics, strong initial operational results and production growth outlook. This asset is expected to generate approximately $275 to $350 million of net operating income less capital expenditures in 2022 at US$65/bbl to US$75/bbl WTI and production of approximately 37,000 boe/d on average, up from approximately 30,000 boe/d when it originally entered the play. The Company now expects to repay the entire cash portion of the Kaybob Duvernay acquisition by year-end 2021.

Shareholder Returns

The Company's Board of Directors has approved and declared a first quarter 2022 dividend of $0.045 per share to be paid on April 1, 2022 to shareholders of record on March 15, 2022, which represents a 50 percent increase from its fourth quarter 2021 dividend. On an annualized basis, this equates to a dividend payment of $0.18 per share. The Company's previously announced fourth quarter 2021 dividend of $0.03 per share is scheduled to be paid on January 4, 2022.

The new dividend level equates to a payout ratio of approximately seven percent of Crescent Point's expected 2022 adjusted funds flow at US$50/bbl WTI. This payout ratio provides dividend sustainability at lower commodity prices, with the ability to grow over time. It also provides flexibility, allowing the Company to continue to prioritize its balance sheet by allocating the majority of its near-term excess cash flow to debt repayment.

In addition to increasing its base dividend, Crescent Point also plans to allocate up to $100 million to share repurchases over the following six months. The Company believes the current value of its common shares does not reflect its underlying fundamental value and that share repurchases provide an attractive opportunity to improve Crescent Point's per share metrics. The planned share repurchases, which equate to over three percent of the Company's current market capitalization, are expected to be partially completed under Crescent Point's existing normal course issuer bid ("NCIB") which expires in March 2022. The Company plans to renew its NCIB with the Toronto Stock Exchange in first quarter 2022.

Crescent Point expects to fully fund its 2022 capital expenditures budget and planned return of capital to shareholders at a low oil price of approximately US$40/bbl WTI. Assuming US$65/bbl to US$75/bbl WTI, the Company expects to generate excess cash flow of approximately $750 million to $1.0 billion in 2022, prior to dividends and expected share repurchases, providing Crescent Point with significant flexibility to create additional shareholder value in the current oil price environment. As the Company continues to strengthen its balance sheet it will look to further increase its return of capital offering to shareholders in the context of its capital allocation framework.

Approximately 50 percent of Crescent Point's oil and liquids production in 2022, net of royalty interest, is now hedged to further protect its balance sheet and expected excess cash flow generation. Crescent Point's leverage ratio is expected to be at or below 1.0 times net debt to adjusted funds flow in early 2022, based on current forward strip commodity prices.

Credit Facility Renewals

During fourth quarter 2021, Crescent Point successfully renewed and extended its unsecured, covenant-based credit facilities with a maturity date of November 2025. Given its significant unutilized credit capacity, the Company downsized its credit facilities to $2.3 billion, better aligning the facilities with the size of the organization while reducing the carrying cost of maintaining undrawn credit capacity. Crescent Point expects to have an unutilized credit capacity of approximately $1.8 billion at year-end 2021.

Related Categories :

Capital Expenditure - 2022

More Capital Expenditure - 2022 News

-

Capex Plans Jump After 2Q: Nearly 30 E&P Companies Raise 2022 Budgets -

-

Civeo Corp. Second Quarter 2022 Results; Raises Guidances

-

2022 Guidance Growth: Several Operators Bolster Capex, Production Outlook -

-

PDC Updates Budget Following Great Western Deal; Adds $50MM

-

Enerplus Bets on Bakken for 2022; Drill 50 Wells, 1.5 Rigs -

Canada News >>>

-

Why $90 Oil Isn’t Bringing Back the Rigs -

-

Q1 A&D Transactions Jump to $30B , While Deal Flow Was Down 40%

-

Western Canada Upstream M&A: Q1 2026 Transaction Report

-

Wright to U.S. Oil Industry: The Price Signal Is Telling You to Drill

-

This Operator Will Chop it's 2026 Rig Count From 34 to 24 -

North America News >>>

-

A Quiet Capital Pattern Is Forming in North American Upstream — and Almost No One Is Talking About It -

-

Canadan E&P 2026 Program Calls for 448 Net Wells, Up 24% vs. 2025 Plan -

-

EIA’s “Glut” Calls: The 2025 Surplus Claim — and How 2021–2024 Forecasts Actually Held Up

-

Permian E&P Bucking The Trend; Plan to Increasing Drilling & Fracs in 2026 -

-

Whitecap Details 2026 Duvernay & Montney Program