Quarterly / Earnings Reports | Fourth Quarter (4Q) Update | Financial Results | Capital Markets | Capital Expenditure | Capital Expenditure - 2021

DCP Midstream Fourth Quarter, Full Year 2020 Results

DCP Midstream LP reported its results for Q4 and full year 2020.

Highlights:

- For the quarter and year ended December 31, 2020, DCP generated net income (loss) attributable to partners of $86 million and $(306) million, net cash provided by operating activities of $308 million and $1,099 million, adjusted EBITDA of $289 million and $1,252 million, and distributable cash flow of $178 million and $850 million.

- Generated $85 million and $237 million of excess free cash flow for the quarter and year ended December 31, 2020, after fully funding $81 million and $406 million in distributions and $12 million and $205 million in growth capital, respectively.

- Utilized $237 million of excess free cash flow and positive working capital to reduce debt by $300 million in 2020, including $125 million in the fourth quarter, achieving a bank leverage of 3.9 times for the year ended December 31, 2020.

- Fourth quarter costs were down $15 million compared to the same period in 2019, resulting in a 14%, or $145 million, annualized reduction compared to 2019, driven by DCP 2.0 transformation efforts and workforce and operational efficiencies.

- Total capital in 2020, including all sustaining and growth capital, was reduced by 74% compared to 2019.

- Conserved over $1.1 billion of cash flow via capital, distribution, and cost reductions compared to 2019, to secure liquidity, generate excess free cash flow, and reduce debt.

- Logistics and Marketing segment accounted for approximately 61% of 2020 adjusted EBITDA, with adjusted segment EBITDA growing 10% year over year, driven by a full year of Gulf Coast Express, the expansions on Front Range and Texas Express, and NGL Marketing, partially offset by lower Guadalupe earnings.

- Brought the 225 MMcf/d Latham 2 Offload online in the DJ Basin at the end of the fourth quarter.

Wouter van Kempen, chairman, president, and CEO, said: "Our team demonstrated tremendous execution in the face of 2020's challenges through early and impactful action to generate $237 million of excess free cash flow and sustainably lower our costs by $145 million, all while maintaining health and safety, improving reliability, and lowering emissions. We are taking a conservative approach to our 2021 volumes and commodity pricing outlook as a result of continued uncertainty driven by COVID-19 and demand recovery timing. We are committed to continuing the momentum established in 2020 by growing excess free cash flow by over 60% in 2021, maintaining our cost reductions, retiring debt, and remaining focused on our operational excellence."

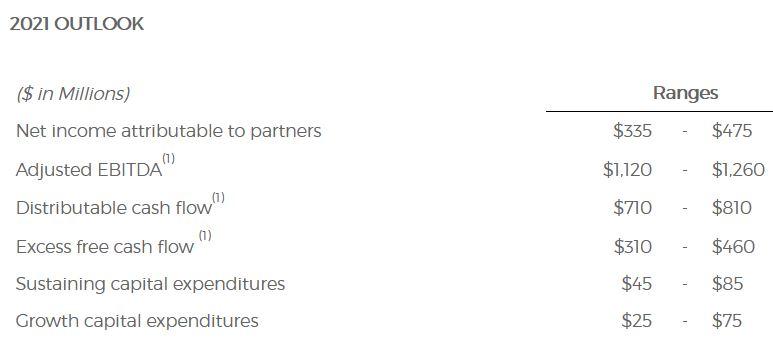

DCP estimates the following 2021 annualized commodity sensitivities, including the effects of hedging:

DCP's 2021 guidance expectations include the following assumptions:

- Sustaining 2020 cost reductions via DCP 2.0 transformation efforts

- No capital markets needs

- Absolute debt reduction while maintaining bank leverage ratio around 4.0 times

- Conservative commodity price deck

- Industry overbuild driving margin compression in both segments

- Slightly increased NGL pipeline volumes due to increased ethane recovery

- Full year earnings from the Cheyenne Connector

- Decreasing Guadalupe earnings as a result of tighter price spreads

- Overall Gathering and Processing volumes slightly declining compared to 2020

- Maintain stable distribution at $1.56 per common unit (annualized)

Distributions

On January 21, 2021, DCP announced a quarterly common unit distribution of $0.39 per limited partner unit. This distribution remains unchanged from the previous quarter.

DCP generated distributable cash flow of $178 million and $850 million for the quarter and year ended December 31, 2020, respectively. Distributions declared were $81 million and $325 million for the quarter and year ended December 31, 2020, respectively.

Q4 2020 Operating Results by Segment

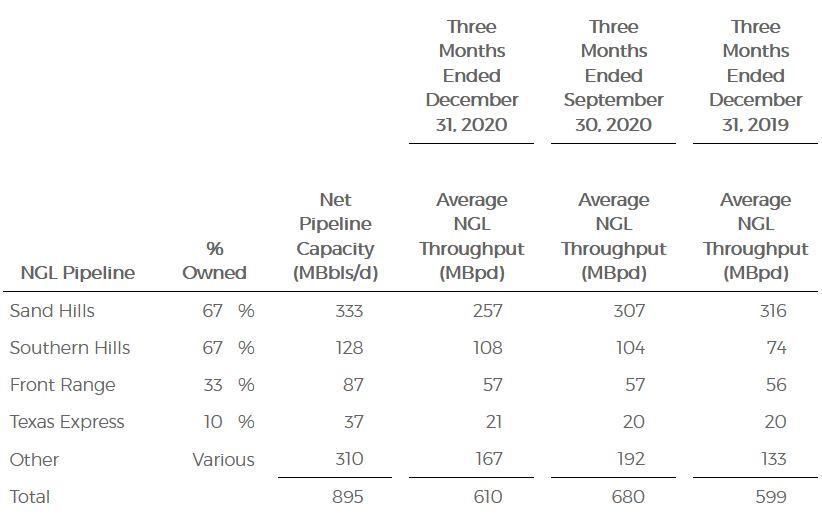

Logistics and Marketing

Logistics and Marketing segment net income attributable to partners for the three months ended December 31, 2020 and 2019 was $158 million and $149 million, respectively.

Adjusted segment EBITDA increased to $183 million for the three months ended December 31, 2020, from $178 million for the three months ended December 31, 2019, reflecting higher earnings from Southern Hills and new earnings from the Cheyenne Connector, put into service in 2020, partially offset by lower earnings from Sand Hills and Guadalupe.

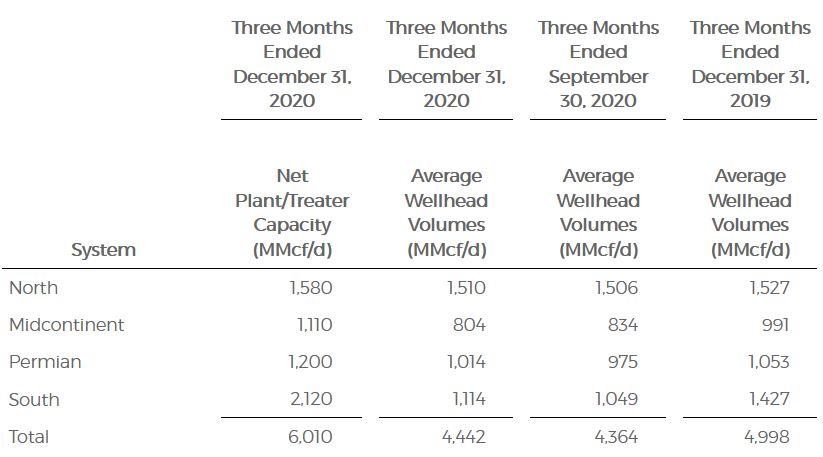

Gathering and Processing segment net income attributable to partners for the three months ended December 31, 2020 and 2019 was $85 million and $12 million, respectively.

Adjusted segment EBITDA decreased to $181 million for the three months ended December 31, 2020, from $190 million for the three months ended December 31, 2019, reflecting lower volumes in the South and Midcontinent regions compared to fourth quarter 2019, partially offset by lower operating costs.

The following table represents volumes for the Gathering and Processing segment:

Credit Facilities & Debt

DCP has two credit facilities with up to $1.75 billion of total capacity. Proceeds from these facilities can be used for working capital requirements and other general partnership purposes including growth and acquisitions.

- DCP has a $1.4 billion senior unsecured revolving credit agreement, or the Credit Agreement, that matures on December 9, 2024. As of December 31, 2020, total available capacity under the Credit Agreement was $1,390 million net of $10 million of letters of credit.

- DCP has an accounts receivable securitization facility that provides up to $350 million of borrowing capacity that matures August 12, 2022. As of December 31, 2020, DCP had $350 million of outstanding borrowings under the accounts receivable securitization facility.

As of December 31, 2020, DCP had $5,625 million of total consolidated principal debt outstanding, with the next maturity in September 2021. The total debt outstanding includes $550 million of junior subordinated notes which are excluded from debt pursuant to DCP's Credit Agreement leverage ratio calculation. For the twelve months ended December 31, 2020, DCP's leverage ratio was 3.9 times. The effective interest rate on DCP's overall debt position, as of December 31, 2020, was 5.26%.

Capital Expenditures

During the quarter and year ended December 31, 2020, DCP had expansion capital expenditures and equity investments totaling $12 million and $205 million, and sustaining capital expenditures totaling $22 million and $45 million, respectively.

Gathering and Processing Project Update

The Latham 2 offload entered into service in the fourth quarter of 2020 and adds up to 225 MMcf/d of incremental DJ Basin processing capacity.

Related Categories :

Fourth Quarter (4Q) Update

More Fourth Quarter (4Q) Update News

-

Apa Corp : Doing More With Less

-

Permian Resources to Grow Production 6% in 2026

-

Endeavor Talks 2023 Development Program; Rigs, Frac Crews -

-

Crescent Energy 4Q, Full Year 2022 Results; Maintenance Capital for 2023

-

W&T Offshore Fourth Quarter, Full Year 2022 Results; 2023 Guidance

United States News >>>

-

A Quiet Capital Pattern Is Forming in North American Upstream — and Almost No One Is Talking About It -

-

EIA’s “Glut” Calls: The 2025 Surplus Claim — and How 2021–2024 Forecasts Actually Held Up

-

New E&P Scores Capital; Heading To the MidCon Region -

-

2025 Forecast : Dangerous Time Ahead -

-

Petrus Resources Ltd. First Quarter 2023 Results

4.jpg&new_width=60&new_height=60&imgsize=false)