Top Story | Capital Markets | Capital Expenditure | Capex Increase | Capital Expenditure - 2021

Enerplus Ups 2021 Capex, Production Outlook After Striking Bakken Deal

Enerplus Corp. has updated its 2021 guidance after announcing a $312MM acquisition deal in the Bakken (the seller is Hess Corp.). Earlier this year, Enerplus also closed on its acquisition of Bakken-focused Bruin E&P.

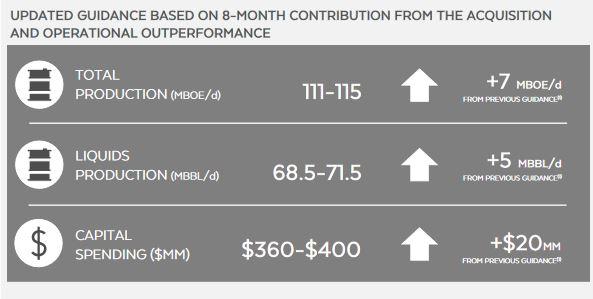

Enerplus is increasing its 2021 production guidance to 111,000 to 115,000 BOE per day (up 7% at the midpoint from 103,500 to 108,500 BOE per day), including 68,500 to 71,500 barrels per day of liquids (from 63,000 to 67,000 barrels per day).

The increased production guidance was also driven by strong operating performance in North Dakota and higher than expected production in the Marcellus through the first three months of the year.

Capital spending in 2021 is revised to $360 to $400 million (from $335 to $385 million) in connection with the acquired assets - an increase of 9% at the midpoint.

The Company's 2021 Bakken oil price differential outlook is unchanged at $3.25 per barrel below WTI, which assumes the Dakota Access Pipeline ("DAPL") continues to operate. In the event DAPL is required to cease operations, Enerplus expects sufficient rail egress to be available, however, Bakken oil price differentials would be expected to widen reflecting rail economics. The Company estimates this would result in a realized 2021 differential of approximately $6.00 per barrel below WTI, assuming eight months of wider differentials if DAPL cannot operate. The impact to Enerplus' corporate netback in this scenario is estimated to be approximately $0.90 per BOE. The Acquisition is expected to continue to provide attractive financial returns at a wider differential, as outlined above.

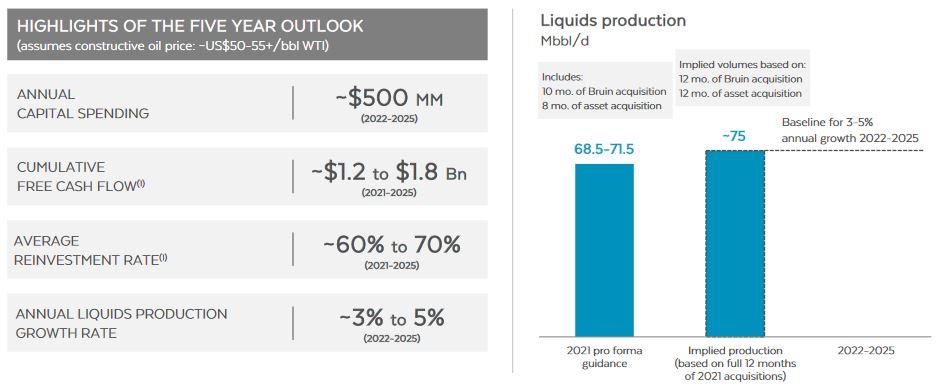

Five Year Outlook

Enerplus also updated its five year plan as follows:

In connection with its five-year outlook, Enerplus has provided a capital allocation framework with the following key principles:

- Maintain low financial leverage: Target a long-term net debt to adjusted funds flow ratio of less than 1.0x.

- Committed to free cash flow generation: Target a long-term capital spending reinvestment rate of less than 75% of annual adjusted funds flow.

- Return capital to shareholders: Sustainably grow the Company's base dividend supported by an increasing cash flow base. Consider share repurchases to further enhance the return of capital to shareholders.

To highlight Enerplus' financial sustainability and robust free cash flow growth potential, the Company has provided an outlook through 2025. Assuming a constructive commodity price environment (WTI oil prices at approximately US$50 to $55 per barrel or higher), the Company projects annual capital spending of approximately $500 million from 2022 to 2025 focused on generating substantial levels of free cash flow. Under this capital spending plan, cumulative free cash flow is estimated at $1.2 to $1.8 billion between 2021 and 2025 based on a US$50 to $55 per barrel WTI crude oil price and US$2.75 per Mcf NYMEX natural gas price.(2) This is expected to result in an average capital spending reinvestment rate of approximately 60% to 70% of adjusted funds flow over the period. Enerplus projects 3% to 5% annual liquids production growth from 2022 to 2025 based on this outlook. This growth rate is based on approximately 75,000 barrels per day, being the Company's implied liquids production in 2021 assuming a full year contribution from its recent acquisitions.

More Capex Increase News

Whitecap Details 2026 Duvernay & Montney Program

Whitecap Resources reported strong third quarter 2025 operating and financial results, marking its first full quarter following the strategic combination with Veren that closed on May 12, 2025.…

Capex Plans Jump After 2Q: Nearly 30 E&P Companies Raise 2022 Budgets

In their second quarter reports, a large number of E&P companies made sizable increases to their 2022 capital spending plans. A total of 29 companies increased their 2022…

Riley Exploration Permian Second Quarter 2022 Results; Ups 2022 Capex

Riley Exploration Permian, Inc. reported financial and operating results for the fiscal third quarter ended June 30, 2022. Highlights: Averaged oil production of 8.4 MBbls per day, which…

California Resources Second Quarter 2022 Results

California Resources Corp. reported second quarter 2022 operational and financial results. The company also announced the formation of a joint venture with Brookfield Renewable, creating a carbon management…

Murphy Oil Second Quarter 2022 Results

Murphy Oil Corp. announced its financial and operating results for the second quarter ended June 30, 2022. Murphy reported net income attributable to Murphy of $351 million, or…

Rockies News

Why $90 Oil Isn’t Bringing Back the Rigs

Higher oil prices are not translating cleanly into a drilling response across U.S. shale, and company disclosures are starting to show why. The issue is not simply capital…

Q1 A&D Transactions Jump to $30B , While Deal Flow Was Down 40%

The first quarter of 2026 has officially defined the "Barbell Era" of American oil and gas. While the total number of deals plummeted by 46% YoY (dropping to…

Wright to U.S. Oil Industry: The Price Signal Is Telling You to Drill

Energy Secretary Chris Wright stood in front of the largest gathering of oil executives in the world this morning and delivered a message that was equal parts market…

This Operator Will Chop it's 2026 Rig Count From 34 to 24

ConocoPhillips is setting up 2026 as a lower-intensity, more efficient operating year — with the clearest proof coming from the Lower 48 activity reset following the Marathon integration.…

A Quiet Capital Pattern Is Forming in North American Upstream — and Almost No One Is Talking About It

A handful of recent transactions and capital raises point to a subtle pattern in North American upstream—one that is easy to miss because each event, on its own,…

Williston Basin News

Permian E&P Bucking The Trend; Plan to Increasing Drilling & Fracs in 2026

Occidental’s 2025 U.S. onshore program is centered on the Permian, with ~$3.5B of Permian CapEx and ~$0.8B in the Rockies, totaling ~$4.3B. This supports ~15 net rigs in…

Bakken Midstream Project shelved; as future growth projects thin

Hess Midstream highlighted continued throughput growth across its Williston Basin (Bakken/Three Forks) systems, signaling higher utilization in gas gathering and processing. For producers, the only forward-looking capacity signal…

Japex Enters DJ Basin with Acquistion of Verdad

Japan Petroleum Exploration Co., Ltd. (JAPEX) has announced a major expansion into North American shale with a $1.3 billion acquisition of Verdad Resources Intermediate Holdings LLC (VRIH), marking…

Dallas Fed Energy Survey: What Oil and Gas Executives Are Really Saying

The latest Dallas Fed Energy Survey shows a U.S. oil and gas industry that is not collapsing—but is clearly constrained. Executives are operating in a defensive posture, focused…

Large E&P Adds Second Completions Crew and Accelerates 4-Mile Lateral Program

Chord Energy extended its 2025 execution streak in 3Q25, delivering oil volumes above the midpoint of guidance while keeping E&P and other capital spending below the midpoint. The…